EX-99.1

Published on September 13, 2013

Exhibit 99.1

|

|

September 2013 |

|

|

When used in this press release or other written or oral communications, statements which are not historical in nature, including those containing words such as will, believe, expect, anticipate, estimate, plan, continue, intend, should, may or similar expressions, are intended to identify forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and, as such, may involve known and unknown risks, uncertainties and assumptions. Statements regarding the following subjects, among others, may be forward-looking: changes in interest rates and the market value of MFAs MBS; changes in the prepayment rates on the mortgage loans securing MFAs MBS; changes in the default rates and managements assumptions regarding default rates on the mortgage loans securing MFAs Non-Agency MBS; MFAs ability to borrow to finance its assets and the terms, including the cost, maturity and other terms, of any such borrowing; implementation of or changes in government regulations or programs affecting MFAs business; MFA's estimates regarding taxable income the actual amount of which is dependent on a number of factors, including, but not limited to, changes in the amount of interest income and financing costs, the method elected by the Company to accrete the market discount on Non-Agency MBS and the extent of prepayments, realized losses and changes in the composition of MFA's Agency MBS and Non-Agency MBS portfolios that may occur during the applicable tax period, including gain or loss on any MBS disposals; the timing and amount of distributions to stockholders, which are declared and paid at the discretion of MFA's Board of Directors and will depend on, among other things, MFA's taxable income, its financial results and overall financial condition and liquidity, maintenance of its REIT qualification and such other factors as the Board deems relevant; MFAs ability to maintain its qualification as a REIT for federal income tax purposes; MFAs ability to maintain its exemption from registration under the Investment Company Act of 1940, as amended (or the Investment Company Act), including statements regarding the Concept Release issued by the SEC relating to interpretive issues under the Investment Company Act with respect to the status under the Investment Company Act of certain companies that are in engaged in the business of acquiring mortgages and mortgage-related interests; and risks associated with investing in real estate assets, including changes in business conditions and the general economy. These and other risks, uncertainties and factors, including those described in the annual, quarterly and current reports that MFA files with the Securities and Exchange Commission, could cause MFAs actual results to differ materially from those projected in any forward-looking statements it makes. All forward-looking statements speak only as of the date on which they are made. New risks and uncertainties arise over time and it is not possible to predict those events or how they may affect MFA. Except as required by law, MFA is not obligated to, and does not intend to, update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Forward Looking Statements 2 |

|

|

MFA is an internally managed REIT that seeks to deliver shareholder value through both the generation of distributable income and through asset performance linked to improvement in residential mortgage credit fundamentals. MFA Financial, Inc. 3 |

|

|

Non-Agency MBS selection is driven by credit analysis and expected return. Agency MBS selection is driven by analysis of interest rate sensitivity, prepayment exposure and expected return. Our Strategy is to Identify the Best Investment Opportunities Throughout the Residential MBS Universe 4 |

|

|

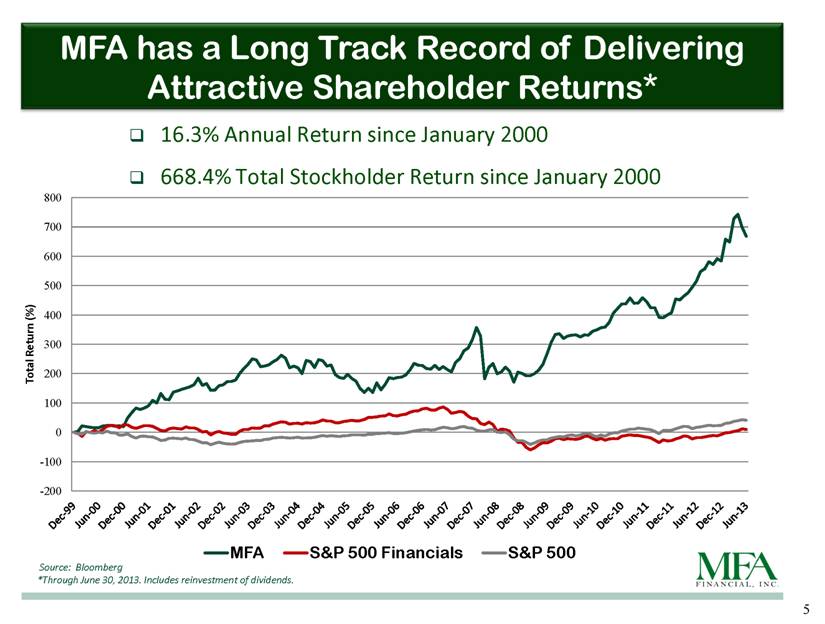

MFA has a Long Track Record of Delivering Attractive Shareholder Returns* Source: Bloomberg *Through June 30, 2013. Includes reinvestment of dividends. 16.3% Annual Return since January 2000 668.4% Total Stockholder Return since January 2000 5 |

|

|

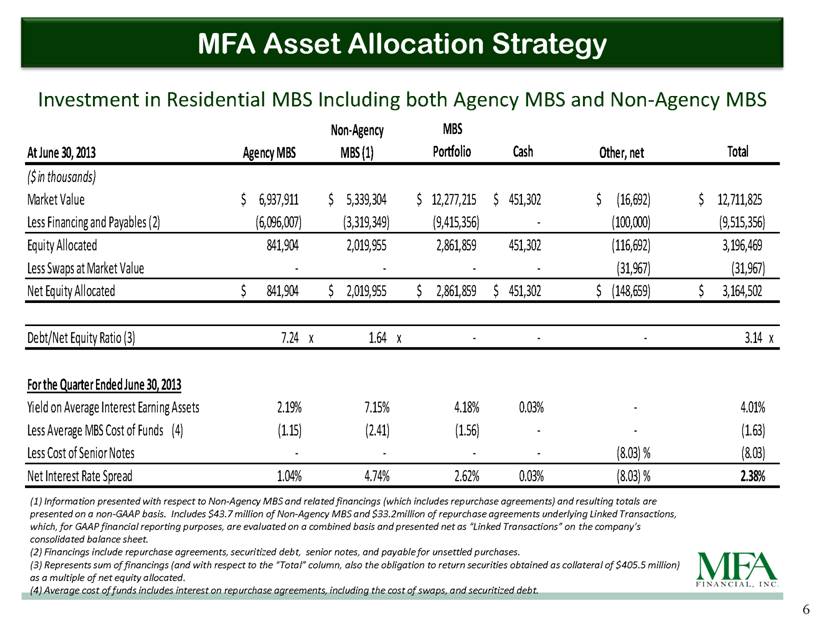

MFA Asset Allocation Strategy Investment in Residential MBS Including both Agency MBS and Non-Agency MBS 6 (1) Information presented with respect to Non-Agency MBS and related financings (which includes repurchase agreements) and resulting totals are presented on a non-GAAP basis. Includes $43.7 million of Non-Agency MBS and $33.2million of repurchase agreements underlying Linked Transactions, which, for GAAP financial reporting purposes, are evaluated on a combined basis and presented net as Linked Transactions on the companys consolidated balance sheet. (2) Financings include repurchase agreements, securitized debt, senior notes, and payable for unsettled purchases. (3) Represents sum of financings (and with respect to the Total column, also the obligation to return securities obtained as collateral of $405.5 million) as a multiple of net equity allocated. (4) Average cost of funds includes interest on repurchase agreements, including the cost of swaps, and securitized debt. At June 30, 2013 MBS Portfolio Cash Total ($ in thousands) Market Value $ 6,937,911 $ 5,339,304 $ 12,277,215 $ 451,302 $ (16,692) $ 12,711,825 Less Financing and Payables (2) (6,096,007) (3,319,349) (9,415,356) - (100,000) (9,515,356) Equity Allocated 841,904 2,019,955 2,861,859 451,302 (116,692) 3,196,469 Less Swaps at Market Value - - - - (31,967) (31,967) Net Equity Allocated $ 841,904 $ 2,019,955 $ 2,861,859 $ 451,302 $ (148,659) $ 3,164,502 Debt/Net Equity Ratio (3) 7.24 x 1.64 x - - - 3.14 x Yield on Average Interest Earning Assets 2.19% 7.15% 4.18% 0.03% - 4.01% Less Average MBS Cost of Funds (4) (1.15) (2.41) (1.56) - - (1.63) Less Cost of Senior Notes - - - - (8.03) % (8.03) Net Interest Rate Spread 1.04% 4.74% 2.62% 0.03% (8.03) % 2.38% For the Quarter Ended June 30, 2013 Agency MBS Non-Agency MBS (1) Other, net |

|

|

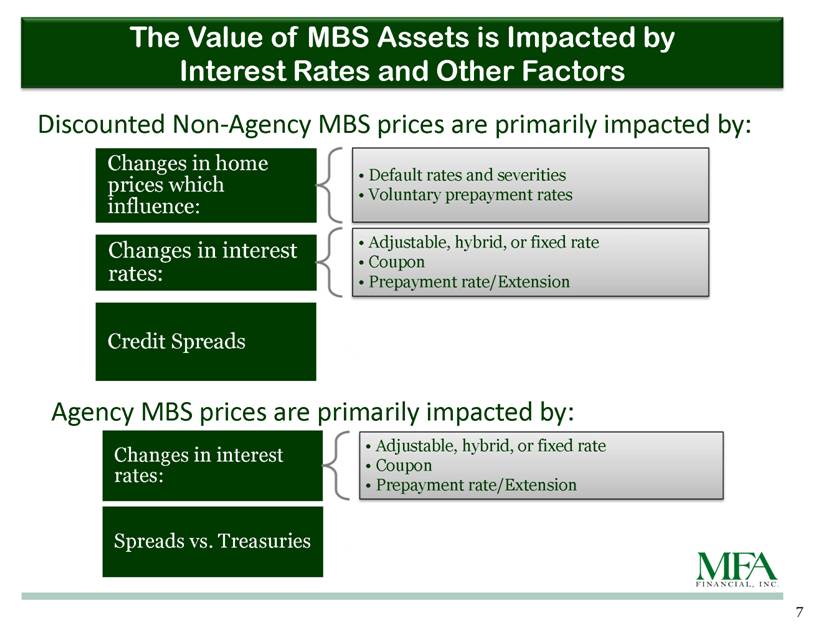

7 The Value of MBS Assets is Impacted by Interest Rates and Other Factors Discounted Non-Agency MBS prices are primarily impacted by: Agency MBS prices are primarily impacted by: |

|

|

8 Interest Rate Strategy MFAs estimated effective duration, which is the measure of price sensitivity to changes in interest rates, has been reduced from approximately 1.70% as of June 30, 2013 to approximately 0.90% as of August 31, 2013. This has been achieved through: The addition of longer term swaps Shorting 15 Year TBAs Select asset sales Acquisition of lower duration assets |

|

|

9 MFAs Interest Rate Sensitivity Assets Market Value Average Coupon Duration Non-Agency ARMs (12 months or less MTR) $2,958 3.09% 0.5 Non-Agency Hybrid (12-48 MTR) $655 5.19% 1.0 Non-Agency Fixed Rate $1,524 5.81% 3.5 Agency ARMs (12 months or less MTR) $1,203 2.92% 0.9 Agency ARMs (12-120 MTR) $3,000 3.47% 2.5 Agency 15 Year Fixed Rate (2.5 CPN) $2,572 3.15% 4.3 Cash $383 0.0 TOTAL ASSETS $12,295 2.2 Cash Flow Notional Amount Duration Swaps (Less than 3 years) $1,479 -1.1 Swaps (3-6 years) $1,000 -4.1 Swaps (6-10 years) $1,400 -6.5 TBA Short Positions $350 -5.0 TOTAL $4,229 -4.0 Net Duration 0.9 $ in millions, data as of 8/30/13 |

|

|

MFA owns approximately $5.3 billion market value ($6.3 billion face amount) of Non-Agency MBS, with an average amortized cost of 74% of par. In the second quarter, these assets generated a loss-adjusted yield of 7.15% on an unlevered basis. Over the past year, we have lowered our estimate of future losses within MFAs Non-Agency MBS portfolio due to a combination of both home price appreciation and mortgage amortization. Accordingly, $224 million has been transferred from credit reserve to accretable discount in the year ended June 30, 2013. This increase in accretable discount will be realized in income over the life of the Non-Agency MBS. *Information presented as of June 30, 2013. MFA Strategy - Non-Agency MBS Significant Investment in Non-Agency MBS* 10 |

|

|

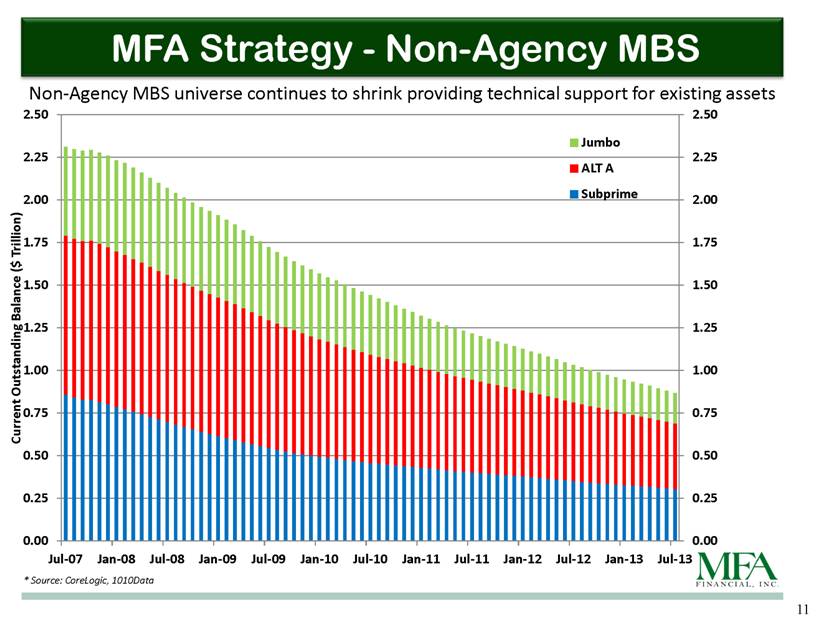

Non-Agency MBS universe continues to shrink providing technical support for existing assets MFA Strategy - Non-Agency MBS * Source: CoreLogic, 1010Data 11 |

|

|

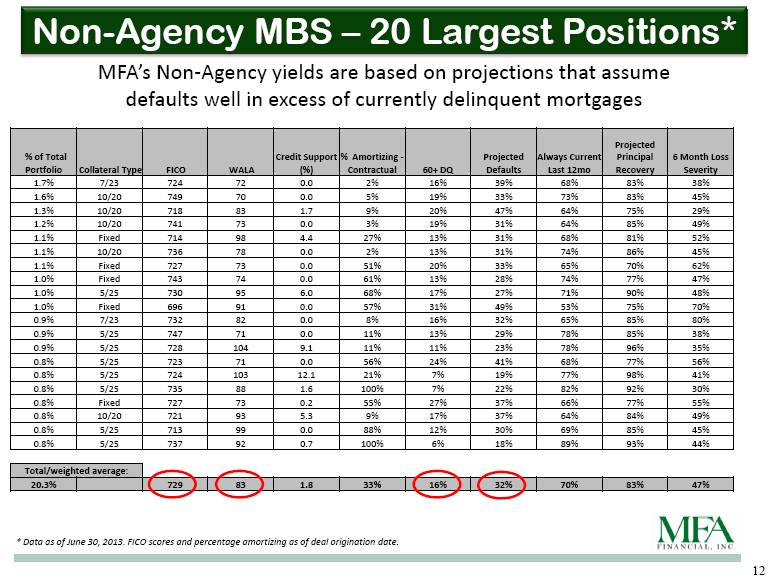

Data as of June 30, 2013. FICO scores and percentage amortizing as of deal origination date. Non-Agency MBS 20 Largest Positions* MFAs Non-Agency yields are based on projections that assume defaults well in excess of currently delinquent mortgages 12 % of Total Portfolio Collateral Type FICO WALA Credit Support (%) % Amortizing - Contractual 60+ DQ Projected Defaults Always Current Last 12mo Projected Principal Recovery 6 Month Loss Severity 1.7% 7/23 724 72 0.0 2% 16% 39% 68% 83% 38% 1.6% 10/20 749 70 0.0 5% 19% 33% 73% 83% 45% 1.3% 10/20 718 83 1.7 9% 20% 47% 64% 75% 29% 1.2% 10/20 741 73 0.0 3% 19% 31% 64% 85% 49% 1.1% Fixed 714 98 4.4 27% 13% 31% 68% 81% 52% 1.1% 10/20 736 78 0.0 2% 13% 31% 74% 86% 45% 1.1% Fixed 727 73 0.0 51% 20% 33% 65% 70% 62% 1.0% Fixed 743 74 0.0 61% 13% 28% 74% 77% 47% 1.0% 5/25 730 95 6.0 68% 17% 27% 71% 90% 48% 1.0% Fixed 696 91 0.0 57% 31% 49% 53% 75% 70% 0.9% 7/23 732 82 0.0 8% 16% 32% 65% 85% 80% 0.9% 5/25 747 71 0.0 11% 13% 29% 78% 85% 38% 0.9% 5/25 728 104 9.1 11% 11% 23% 78% 96% 35% 0.8% 5/25 723 71 0.0 56% 24% 41% 68% 77% 56% 0.8% 5/25 724 103 12.1 21% 7% 19% 77% 98% 41% 0.8% 5/25 735 88 1.6 100% 7% 22% 82% 92% 30% 0.8% Fixed 727 73 0.2 55% 27% 37% 66% 77% 55% 0.8% 10/20 721 93 5.3 9% 17% 37% 64% 84% 49% 0.8% 5/25 713 99 0.0 88% 12% 30% 69% 85% 45% 0.8% 5/25 737 92 0.7 100% 6% 18% 89% 93% 44% Total/weighted average: 20.3% 729 83 1.8 33% 16% 32% 70% 83% 47% |

|

|

13 A combination of low mortgage rates, rising multifamily rents, limited housing supply, capital flows into own-to-rent purchases and demographic driven U.S. household formation, has led to price appreciation on a nationwide basis. MFA Strategy Non-Agency MBS *Includes distressed sales Source: CoreLogic, 1010Data |

|

|

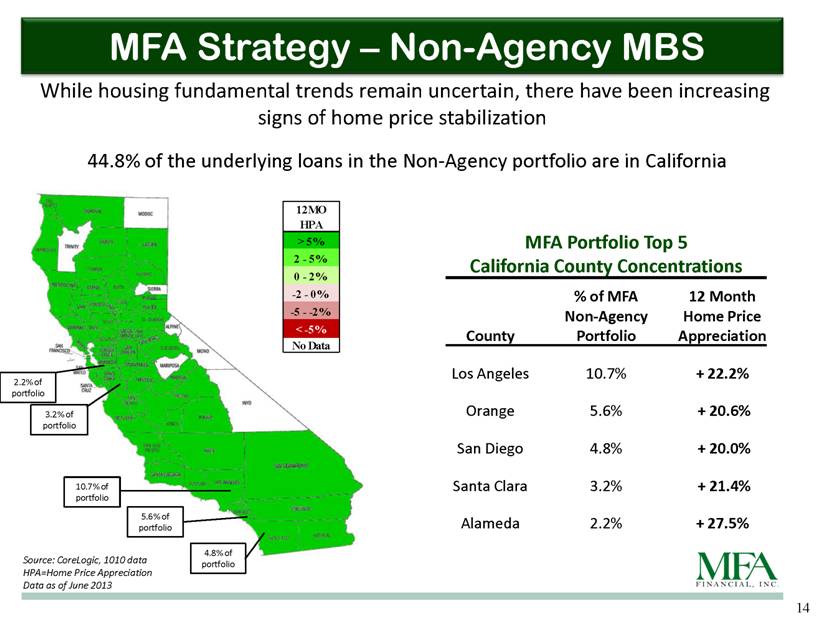

MFA Strategy Non-Agency MBS 14 10.7% of portfolio 5.6% of portfolio 4.8% of portfolio 3.2% of portfolio 2.2% of portfolio Source: CoreLogic, 1010 data HPA=Home Price Appreciation Data as of June 2013 MFA Portfolio Top 5 California County Concentrations County % of MFA Non-Agency Portfolio 12 Month Home Price Appreciation Los Angeles 10.7% + 22.2% Orange 5.6% + 20.6% San Diego 4.8% + 20.0% Santa Clara 3.2% + 21.4% Alameda 2.2% + 27.5% While housing fundamental trends remain uncertain, there have been increasing signs of home price stabilization 44.8% of the underlying loans in the Non-Agency portfolio are in California 12MO HPA > 5% 2 - 5% 0 - 2% -2 - 0% -5 - -2% < -5% No Data |

|

|

15 0.9% of portfolio 0.5% of portfolio 0.5% of portfolio 1.1% of portfolio 1.2% of portfolio MFA Portfolio Top 5 Florida County Concentrations County % of MFA Non-Agency Portfolio 12 Month Home Price Appreciation Miami-Dade 1.2% + 11.8% Broward 1.1% + 12.9% Palm Beach 0.9% + 11.4% Orange 0.5% + 15.7% Hillsborough 0.5% + 9.6% MFA Strategy Non-Agency MBS Florida makes up MFAs second largest Non-Agency geographic concentration with 8.1% of the portfolio Source: CoreLogic, 1010 data HPA=Home Price Appreciation Data as of June 2013 12MO HPA > 5% 2 - 5% 0 - 2% -2 - 0% -5 - -2% < -5% No Data |

|

|

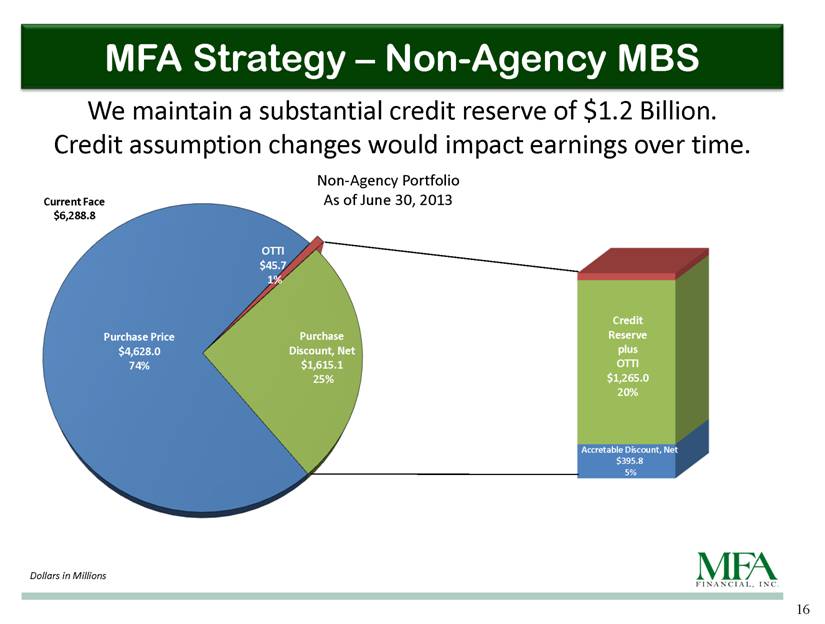

MFA Strategy Non-Agency MBS 16 Non-Agency Portfolio As of June 30, 2013 Current Face $6,288.8 We maintain a substantial credit reserve of $1.2 Billion. Credit assumption changes would impact earnings over time. Dollars in Millions |

|

|

MFA Financial, Inc. Strategy is to identify the best investment opportunities within the Residential MBS universe. Internally managed. 16.3% annual return and 668.4% total return since 2000 (including reinvestment of dividends). Significant $5.3 billion market value investment in Non-Agency MBS sector which generated a 7.15% loss-adjusted unlevered yield in the second quarter. A combination of low mortgage rates, rising multifamily rents, limited housing supply, capital flows into own-to-rent purchases and demographic driven U.S. household formation, has led to price appreciation on a nationwide basis. 17 |