EX-99.2

Published on May 4, 2016

Exhibit 99.2

First Quarter 2016 Earnings Presentation

Forward looking statements 2 When used in this presentation or other written or oral communications, statements which are not historical in nature, including those containing words such as will, believe, expect, anticipate, estimate, plan, continue, intend, should, may or similar expressions, are intended to identify forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and, as such, may involve known and unknown risks, uncertainties and assumptions. Statements regarding the following subjects, among others, may be forward-looking: changes in interest rates and the market value of MFAs MBS; changes in the prepayment rates on the mortgage loans securing MFAs MBS; credit risks underlying MFAs assets, including; changes in the default rates and managements assumptions regarding default rates on the mortgage loans securing MFAs Non-Agency MBS and as related to MFAs residential whole loan portfolio; MFAs ability to borrow to finance its assets and the terms, including the cost, maturity and other terms, of any such borrowing; implementation of or changes in government regulations or programs affecting MFAs business; MFA's estimates regarding taxable income the actual amount of which is dependent on a number of factors, including, but not limited to, changes in the amount of interest income and financing costs, the method elected by the Company to accrete the market discount on Non-Agency MBS and the extent of prepayments, realized losses and changes in the composition of MFA's Agency MBS and Non-Agency MBS portfolios that may occur during the applicable tax period, including gain or loss on any MBS disposals; the timing and amount of distributions to stockholders, which are declared and paid at the discretion of MFA's Board of Directors and will depend on, among other things, MFA's taxable income, its financial results and overall financial condition and liquidity, maintenance of its REIT qualification and such other factors as the Board deems relevant; MFAs ability to maintain its qualification as a REIT for federal income tax purposes; MFAs ability to maintain its exemption from registration under the Investment Company Act of 1940, as amended (or the Investment Company Act), including statements regarding the Concept Release issued by the SEC relating to interpretive issues under the Investment Company Act with respect to the status under the Investment Company Act of certain companies that are in engaged in the business of acquiring mortgages and mortgage-related interests; MFAs ability to successfully implement its strategy to grow its residential whole loan portfolio; expected returns on our investments in non-performing residential whole loans (NPLs), which are affected by, among other things, the length of time required to foreclose upon, sell, liquidate or otherwise reach a resolution of the property underlying the NPL, home price values, amounts advanced to carry the asset (e.g., taxes, insurance, maintenance expenses, etc. on the underlying property) and the amount ultimately realized upon resolution of the asset; and risks associated with investing in real estate assets, including changes in business conditions and the general economy. These and other risks, uncertainties and factors, including those described in the annual, quarterly and current reports that MFA files with the Securities and Exchange Commission, could cause MFAs actual results to differ materially from those projected in any forward-looking statements it makes. All forward-looking statements speak only as of the date on which they are made. New risks and uncertainties arise over time and it is not possible to predict those events or how they may affect MFA. Except as required by law, MFA is not obligated to, and does not intend to, update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Executive summary In this low interest rate environment, we continue to generate attractive returns from residential credit mortgage assets. In the first quarter we generated EPS and dividend per share of $0.20. MFA continued to acquire credit sensitive loans and 3 year step-up RPL/NPL securities in response to attractive investment opportunities. 3

4 Time Period Annualized MFA Shareholder Return (1) Since 2000 14.4% 10 Year 13.0% 5 Year 10.6% Through volatile markets and both interest rate and credit cycles, MFA has generated strong long term returns to investors (1) As of 3/31/16 assuming reinvestment of dividends

Invest in high value-added assets Generate returns from investment in credit sensitive residential mortgage assets MFAs credit assets continue to perform well. Legacy Non-Agency MBS Credit Reserve has been reduced by $23.0 million over the past 12 months. Acquire assets with less interest rate sensitivity 73% of MFA MBS are adjustable, hybrid or step-up Net portfolio duration of 0.55 Maintain staying power and the ability to invest in distressed, less liquid markets Permanent equity capital Debt to Equity Ratio of 3.4x is low enough to accommodate potential changes in marks. MFA is able to invest while other investors may face concerns about capital outflows and potential mark-to-market losses. 5 2016 MFA strategy

First Quarter investment flows Our assets run off, due to amortization, paydowns or sale, allowing reinvestment opportunities in changing interest rate and credit environments. $ in Millions 6 December 31, 2015 1st Quarter Runoff 1st Quarter Acquisitions MTM and other changes March 31, 2016 1st Quarter Change Re-performing and Non-performing Loans $895 $(26) $161 $(6) $1,024 $129 3 Year Step-up RPL/NPL Securities $2,626 $(435)* $302 $3 $2,496 $(130) Credit Risk Transfer Securities $184 $ $29 $3 $216 $32 Legacy Non-Agency MBS $3,795 $(192) $44 $(42) $3,605 $(190) Agency MBS $4,752 $(212) $ $5 $4,545 $(207) * Includes approximately $200 million of bonds redeemed late in March 2016.

MFAs yields and spreads remain attractive 7 First Quarter 2016 Fourth Quarter 2015 Third Quarter 2015 Yield on Interest Earning Assets 4.23% 4.15% 4.05% Net Interest Rate Spread 2.18% 2.22% 2.24% Debt Equity Ratio 3.4x 3.4x 3.3x EPS $0.20 $0.19 $0.20

Yields and spreads by asset type 8 Quarter Ended March 31, 2016 Asset Yield/Return Cost of Funds Net Spread Debt/Net Equity Ratio Agency MBS 2.07 % (1.27)% 0.80% 8.1x Non-Agency MBS 7.61 % (2.86)% 4.75% 2.2x RPL/NPL MBS 3.97 % (2.07)% 1.90% 3.3x RPL Whole Loans 6.00 % (1) (2.80)% 3.20% 0.7x NPL Whole Loans (2) (3.34)% (2) 2.0x Net of 53 bps of servicing costs Residential whole loans held at fair value produce GAAP income/loss based on changes in fair value in the current period and therefore results will vary on a quarter to quarter basis. The company expects to realize returns over time on these investments of 5-7%.

Distributable Income / Items expected to impact future Taxable Income 9 As of March 31, 2016 MFA had undistributed REIT taxable income of $0.17 per share. Undistributed REIT taxable income at the end of the first quarter includes the impact of the unwind of a re-securitization financing structure which generated taxable income (though not GAAP income) of approximately $0.19 per share In addition to the re-securitization unwind, settlement of the Countrywide litigation, which is expected to occur prior to the end of the second quarter, is estimated to generate taxable income of approximately $0.05 per share

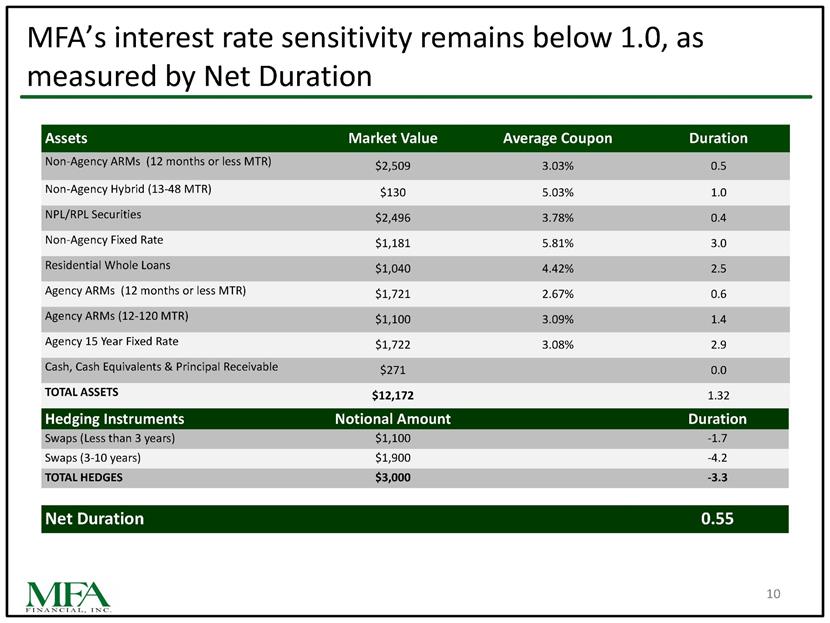

MFAs interest rate sensitivity remains below 1.0, as measured by Net Duration 10 Net Duration0.55 AssetsMarket ValueAverage CouponDuration Non-Agency ARMs (12 months or less MTR)$2,5093.03%0.5 Non-Agency Hybrid (13-48 MTR)$1305.03%1.0 NPL/RPL Securities$2,4963.78%0.4 Non-Agency Fixed Rate$1,1815.81%3.0 Residential Whole Loans$1,0404.42%2.5 Agency ARMs (12 months or less MTR)$1,7212.67%0.6 Agency ARMs (12-120 MTR)$1,1003.09%1.4 Agency 15 Year Fixed Rate$1,7223.08%2.9 Cash, Cash Equivalents & Principal Receivable$2710.0 TOTAL ASSETS$12,1721.32 Hedging InstrumentsNotional AmountDuration Swaps (Less than 3 years)$1,100-1.7 Swaps (3-10 years)$1,900-4.2 TOTAL HEDGES$3,000-3.3

Book value down 4% primarily due to impact of fair value changes in legacy Non-Agency MBS and Swap hedges 11 Book value per common share as of 12/31/15 $7.47 Net income available to common shareholders 0.20 Common dividend declared during the quarter (0.20) Net change attributable to Agency MBS 0.03 Net change attributable to Non-Agency MBS and CRT securities (0.19) Net change in value of swap hedges (0.14) Book value per common share as of 03/31/16 $7.17

First Quarter Non-Agency MBS impact on MFA book value 12 Impact Per Share(1) Impact of change in market prices $(0.12) Realized gains from asset sales: Reallocation from OCI to Retained Earnings $(0.03) Discount Accretion: Primarily income in excess of coupon on Non-Agency MBS purchased at a discount. This income increases amortized cost and lowers unrealized gains $(0.06) Principal Paydowns $0.06 Realized Credit Losses $(0.04) Total $(0.19) (1) Does not include impact of swap hedges.

While economic growth rate is uncertain, there are many positive fundamentals for residential mortgage credit and home prices 13 Strong fundamental and technical support for residential credit assets and home prices Sales of existing homes rose 5.5% in March 2016 to 5.3 million* Median existing single-family home prices are up 5.8% year over year (as of March 2016)* Fewer US homes in foreclosure (as % of homes with mortgages) Seriously delinquent (90+ days) US mortgages continue to decline Foreclosure inventory is down 23.9% year over year (as of February 2016) ** *National Association of Realtors **CoreLogic

Continued growth in Credit Sensitive Loan portfolio 14 Re-Performing and Non-Performing Loan Portfolio $ in Millions At todays market prices, re-performing and non-performing residential mortgage loans generate higher yields than residential MBS. Residential whole loans are qualifying interests for purposes of REIT qualification and 1940 Act Exemption. Significant expected supply March 31, 2016 Dec 31, 2015 Sept 30, 2015 June 30, 2015 March 31, 2015 $1,024 $895 $777 $429 $387

15 Early results indicate returns to date are consistent with our expectation of 5-7% Utilizes the same residential mortgage credit expertise we have employed in Legacy Non-Agency MBS since 2008. Ability to oversee servicing decisions (loan modifications, short sales, etc.) to produce better NPV outcomes. MFA has obtained financing of $589.1 million through three different warehouse borrowing facilities. We are currently negotiating the establishment of a fourth warehouse facility MFA actively manages its loan portfolio through in-house asset management professionals and utilizes third-party special servicers. Credit Sensitive Residential Whole Loans: Growing asset class for MFA

First Quarter RPL/NPL MBS holdings 16 Portfolio yields have increased 3.97% yield in Q1 2016 vs 3.70% yield in Q4 2015 Recent purchases have been at yields above 4.25% Some deals have 24 month step-ups (vs. 36 month step-ups) As of March 31, 2016 Fair Value mm Net Coupon Months to Step-Up Current Credit Support Original Credit Support 3 Month Average Bond CPR Re-Performing MBS $482 3.72% 15 47% 40% 14.2% Non-Performing MBS $2,014 3.79% 23 49% 48% 25.0% Total RPL/NPL MBS $2,496 3.78% 22 48% 47% 23.0%

LTV breakdown of non-delinquent mortgage loans underlying MFAs Legacy Non-Agency MBS These loans are up to date on all required mortgage payments. Underlying loans are ten years seasoned on average. Source: CoreLogic Data as of March 31, 2016

Summary 18 We continue to utilize our expertise to identify and acquire attractive credit sensitive residential mortgage assets. Continued to acquire credit sensitive mortgage loans and 3 Year step-up RPL/NPL securities during the quarter. Our credit sensitive assets continue to perform well. MFA is well positioned for changes in monetary policy and/or interest rates.