EXHIBIT 99.2

Published on August 5, 2021

Exhibit 99.2

Second Quarter 2021 Earnings Presentation

Forward looking statements 2 When used in this presentation or other written or oral communications, statements which are not historical in nature, including those containing words such as “will,” “believe,” “expect,” “anticipate,” “estimate,” “plan,” “continue,” “intend,” “should,” “could,” “would,” “may,” the negative of these words or similar expressions, are intended to identify “forward - looking statements” within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended, and, as such, may involve known and unknown risks, uncertainties and assumptions . These forward - looking statements include information about possible or assumed future results with respect to our business, financial condition, liquidity, results of operations, plans and objectives . Statements regarding the following subjects, among others, may be forward - looking : risks related to the COVID - 19 pandemic, including the pandemic’s effect on the general economy and our business, financial position and results of operations (including, among other potential effects, increased delinquencies and greater than expected losses in our whole loan portfolio) ; changes in interest rates and the market (i . e . , fair) value of MFA’s residential whole loans, MBS and other assets ; changes in the prepayment rates on residential mortgage assets, an increase of which could result in a reduction of the yield on certain investments in MFA’s portfolio and could require MFA to reinvest the proceeds received by it as a result of such prepayments in investments with lower coupons, while a decrease in which could result in an increase in the interest rate duration of certain investments in MFA’s portfolio making their valuation more sensitive to changes in interest rates and could result in lower forecasted cash flows ; credit risks underlying MFA’s assets, including changes in the default rates and management’s assumptions regarding default rates on the mortgage loans in MFA’s residential whole loan portfolio ; MFA’s ability to borrow to finance its assets and the terms, including the cost, maturity and other terms, of any such borrowings ; implementation of or changes in government regulations or programs affecting MFA’s business ; MFA’s estimates regarding taxable income, the actual amount of which is dependent on a number of factors, including, but not limited to, changes in the amount of interest income and financing costs, the method elected by MFA to accrete the market discount on residential whole loans and the extent of prepayments, realized losses and changes in the composition of MFA’s residential whole loan portfolios that may occur during the applicable tax period, including gain or loss on any MBS disposals and whole loan modifications, foreclosures and liquidations ; the timing and amount of distributions to stockholders, which are declared and paid at the discretion of MFA’s Board and will depend on, among other things, MFA’s taxable income, its financial results and overall financial condition and liquidity, maintenance of its REIT qualification and such other factors as MFA’s Board deems relevant ; MFA’s ability to maintain its qualification as a REIT for federal income tax purposes ; MFA’s ability to maintain its exemption from registration under the Investment Company Act of 1940 , as amended (or the “Investment Company Act”), including statements regarding the concept release issued by the Securities and Exchange Commission (“SEC”) relating to interpretive issues under the Investment Company Act with respect to the status under the Investment Company Act of certain companies that are engaged in the business of acquiring mortgages and mortgage - related interests ; MFA’s ability to continue growing its residential whole loan portfolio, which is dependent on, among other things, the supply of loans offered for sale in the market ; expected returns on MFA’s investments in nonperforming residential whole loans (“NPLs”), which are affected by, among other things, the length of time required to foreclose upon, sell, liquidate or otherwise reach a resolution of the property underlying the NPL, home price values, amounts advanced to carry the asset (e . g . , taxes, insurance, maintenance expenses, etc . on the underlying property) and the amount ultimately realized upon resolution of the asset ; targeted or expected returns on MFA’s investments in recently - originated loans, the performance of which is, similar to MFA’s other mortgage loan investments, subject to, among other things, differences in prepayment risk, credit risk and financing cost associated with such investments ; risks associated with MFA’s investments in MSR - related assets, including servicing, regulatory and economic risks, risks associated with our investments in loan originators, risks associated with investing in real estate assets, including changes in business conditions and the general economy and risks associated with the integration of MFA’s recently - completed acquisition of Lima One Holdings, LLC, and the ongoing operation thereof (including, without limitation, unanticipated expenditures relating to or liabilities arising from the transaction and/or the inability to obtain, or delays in obtaining, expected benefits from the transaction) . These and other risks, uncertainties and factors, including those described in the annual, quarterly and current reports that MFA files with the SEC, could cause MFA’s actual results to differ materially from those projected in any forward - looking statements it makes . All forward - looking statements are based on beliefs, assumptions and expectations of MFA’s future performance, taking into account all information currently available . Readers are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date on which they are made . New risks and uncertainties arise over time and it is not possible to predict those events or how they may affect MFA . Except as required by law, MFA is not obligated to, and does not intend to, update or revise any forward - looking statements, whether as a result of new information, future events or otherwise .

Executive summary 3 • Q 2 2021 financial results • Lima One purchase • Continued execution of securitizations • Investment portfolio and asset - based financing composition

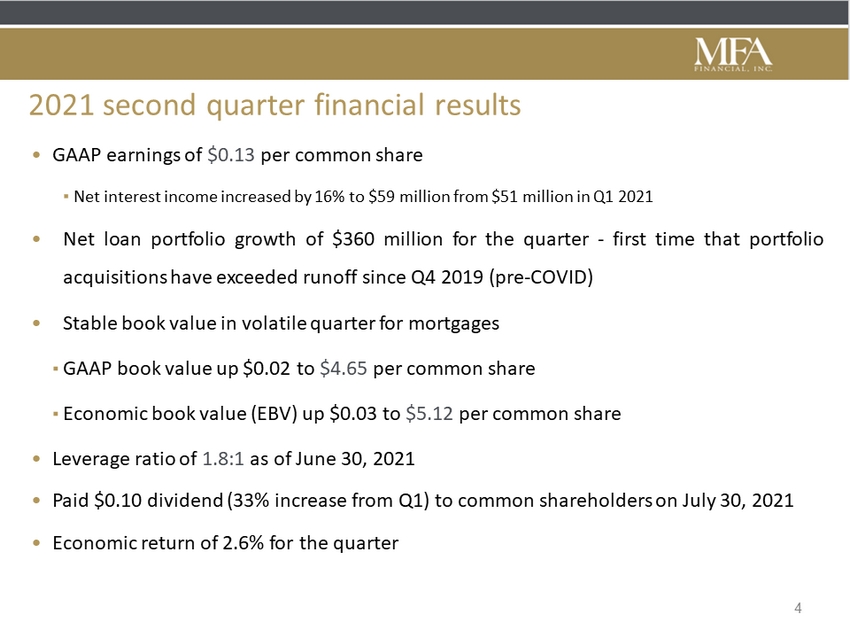

2021 second quarter financial results 4 • GAAP earnings of $ 0 . 13 per common share ▪ Net interest income increased by 16 % to $ 59 million from $ 51 million in Q 1 2021 • Net loan portfolio growth of $ 360 million for the quarter - first time that portfolio acquisitions have exceeded runoff since Q 4 2019 (pre - COVID) • Stable book value in volatile quarter for mortgages ▪ GAAP book value up $ 0 . 02 to $ 4 . 65 per common share ▪ Economic book value (EBV) up $ 0 . 03 to $ 5 . 12 per common share • Leverage ratio of 1 . 8 : 1 as of June 30 , 2021 • Paid $ 0 . 10 dividend ( 33 % increase from Q 1 ) to common shareholders on July 30 , 2021 • Economic return of 2 . 6 % for the quarter

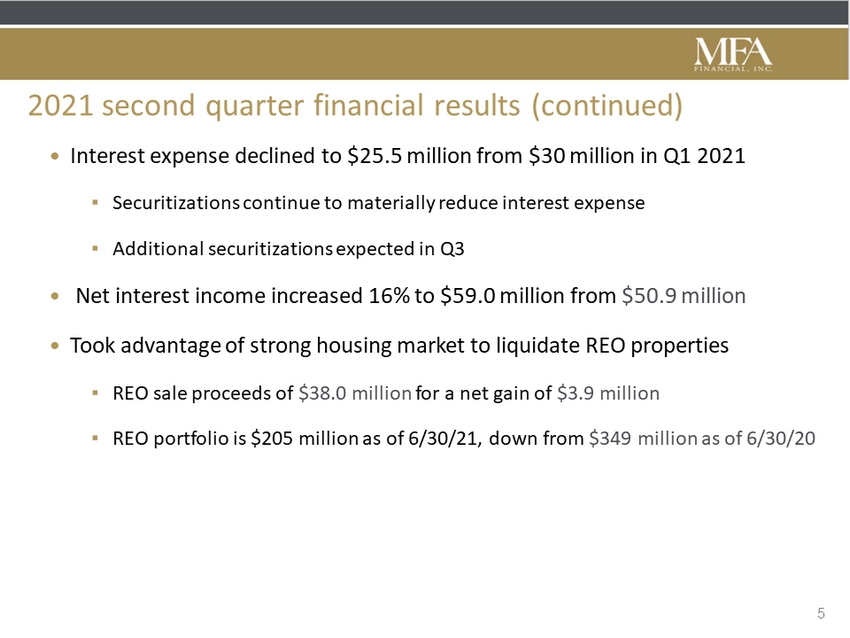

2021 second quarter financial results (continued) • Interest expense declined to $ 25 . 5 million from $ 30 million in Q 1 2021 ▪ Securitizations continue to materially reduce interest expense ▪ Additional securitizations expected in Q 3 • Net interest income increased 16 % to $ 59 . 0 million from $ 50 . 9 million • Took advantage of strong housing market to liquidate REO properties ▪ REO sale proceeds of $ 38 . 0 million for a net gain of $ 3 . 9 million ▪ REO portfolio is $ 205 million as of 6 / 30 / 21 , down from $ 349 million as of 6 / 30 / 20 5

Lima One purchase completed July 1, 2021 6 Closed the purchase of Lima One Capital, a leading nationwide originator and servicer of business purpose loans (BPLs) . • Integration is progressing efficiently • Lima One’s financial results will be consolidated into MFA’s financial results during the third quarter • Lima One is originating at higher than pre - COVID levels • Lima One is on pace to originate over $ 1 . 3 billion of BPLs in 2021 and has substantial growth potential • Improved financing (including securitizations) and access to capital are expected to enhance Lima One profitability • Reliable source of substantial loan production for MFA’s balance sheet

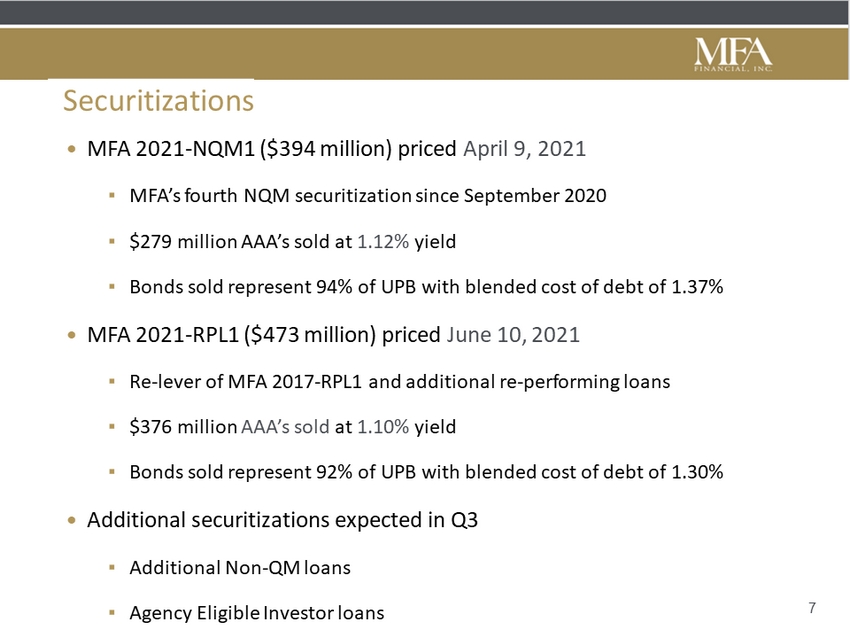

Securitizations 7 • MFA 2021 - NQM 1 ( $ 394 million) priced April 9 , 2021 ▪ MFA’s fourth NQM securitization since September 2020 ▪ $ 279 million AAA’s sold at 1 . 12 % yield ▪ Bonds sold represent 94 % of UPB with blended cost of debt of 1 . 37 % • MFA 2021 - RPL 1 ( $ 473 million) priced June 10 , 2021 ▪ Re - lever of MFA 2017 - RPL 1 and additional re - performing loans ▪ $ 376 million AAA’s sold at 1 . 10 % yield ▪ Bonds sold represent 92 % of UPB with blended cost of debt of 1 . 30 % • Additional securitizations expected in Q 3 ▪ Additional Non - QM loans ▪ Agency Eligible Investor loans

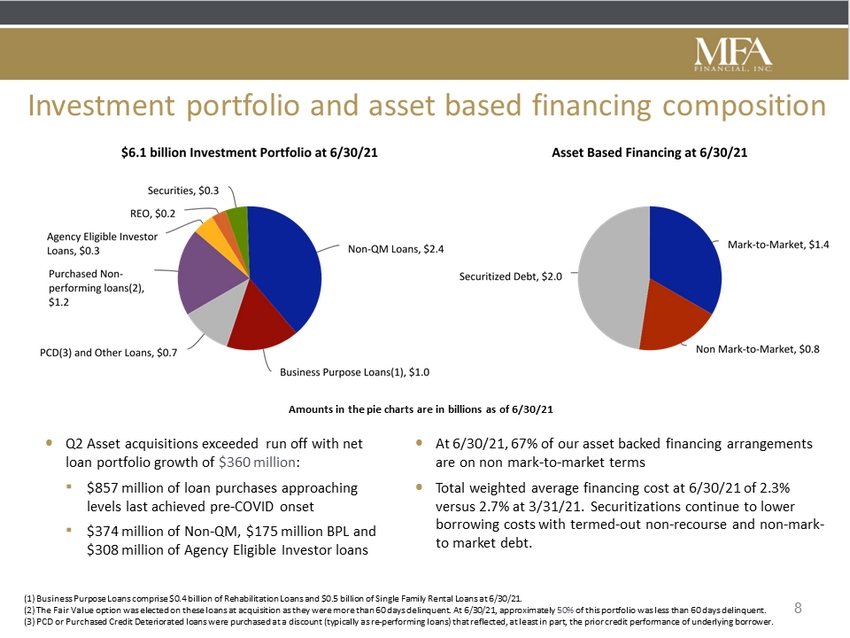

8 • Q2 Asset acquisitions exceeded run off with net loan portfolio growth of $360 million : ▪ $857 million of loan purchases approaching levels last achieved pre - COVID onset ▪ $374 million of Non - QM, $175 million BPL and $308 million of Agency Eligible Investor loans • At 6/30/21, 67% of our asset backed financing arrangements are on non mark - to - market terms • Total weighted average financing cost at 6/30/21 of 2.3% versus 2.7% at 3/31/21. Securitizations continue to lower borrowing costs with termed - out non - recourse and non - mark - to market debt. Amounts in the pie charts are in billions as of 6/30/21 (1) Business Purpose Loans comprise $0.4 billion of Rehabilitation Loans and $0.5 billion of Single Family Rental Loans at 6/ 30/ 21. (2) The Fair Value option was elected on these loans at acquisition as they were more than 60 days delinquent. At 6/30/21, ap pro ximately 50% of this portfolio was less than 60 days delinquent. (3) PCD or Purchased Credit Deteriorated loans were purchased at a discount (typically as re - performing loans) that reflected, a t least in part, the prior credit performance of underlying borrower. Investment portfolio and asset based financing composition

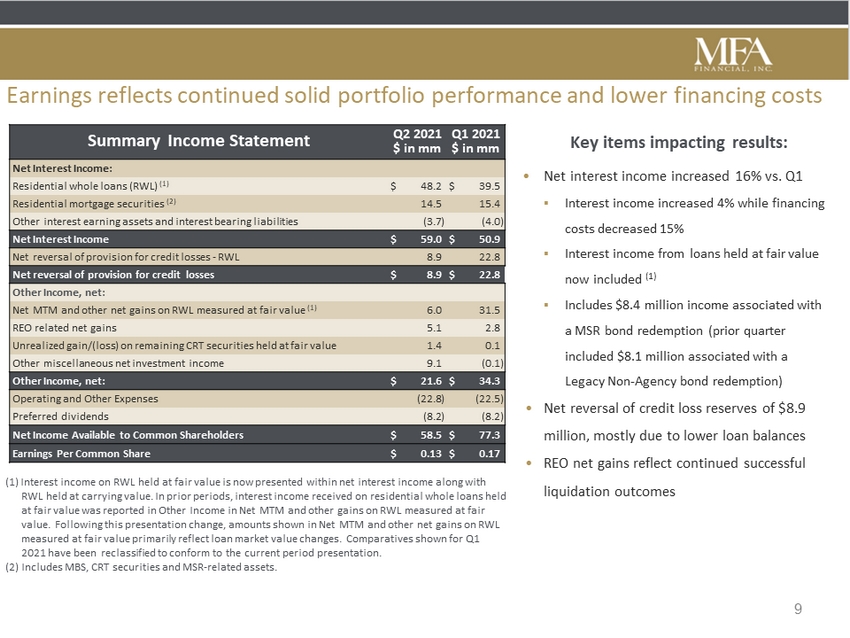

Earnings reflects continued solid portfolio performance and lower financing costs Summary Income Statement Q2 2021 $ in mm Q1 2021 $ in mm Net Interest Income: Residential whole loans (RWL) (1) $ 48.2 $ 39.5 Residential mortgage securities (2) 14.5 15.4 Other interest earning assets and interest bearing liabilities (3.7 ) (4.0 ) Net Interest Income $ 59.0 $ 50.9 Net reversal of provision for credit losses - RWL 8.9 22.8 Net reversal of provision for credit losses $ 8.9 $ 22.8 Other Income, net: Net MTM and other net gains on RWL measured at fair value (1) 6.0 31.5 REO related net gains 5.1 2.8 Unrealized gain/(loss) on remaining CRT securities held at fair value 1.4 0.1 Other miscellaneous net investment income 9.1 (0.1 ) Other Income, net: $ 21.6 $ 34.3 Operating and Other Expenses (22.8 ) (22.5 ) Preferred dividends (8.2 ) (8.2 ) Net Income Available to Common Shareholders $ 58.5 $ 77.3 Earnings Per Common Share $ 0.13 $ 0.17 • Net interest income increased 16% vs. Q1 ▪ Interest income increased 4% while financing costs decreased 15% ▪ Interest income from loans held at fair value now included (1) ▪ Includes $8.4 million income associated with a MSR bond redemption (prior quarter included $8.1 million associated with a Legacy Non - Agency bond redemption) • Net reversal of credit loss reserves of $8.9 million, mostly due to lower loan balances • REO net gains reflect continued successful liquidation outcomes 9 (1) Interest income on RWL held at fair value is now presented within net interest income along with RWL held at carrying value. In prior periods, interest income received on residential whole loans held at fair value was reported in Other Income in Net MTM and other gains on RWL measured at fair value. Following this presentation change, amounts shown in Net MTM and other net gains on RWL measured at fair value primarily reflect loan market value changes. Comparatives shown for Q1 2021 have been reclassified to conform to the current period presentation. (2) Includes MBS, CRT securities and MSR - related assets. Key items impacting results:

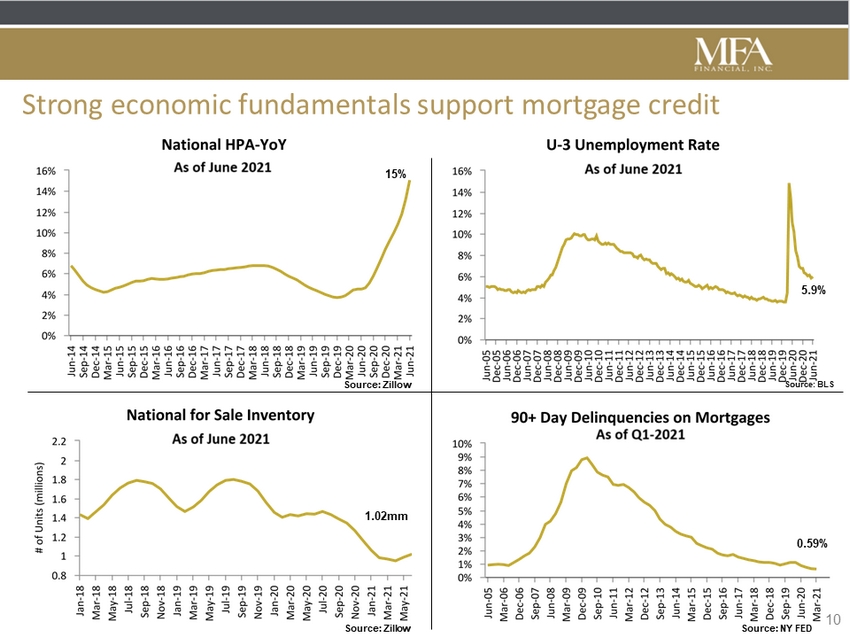

Strong economic fundamentals support mortgage credit 10 15% 5.9% 0.59% 1.02mm Source: Zillow Source: NY FED Source: BLS Source: Zillow

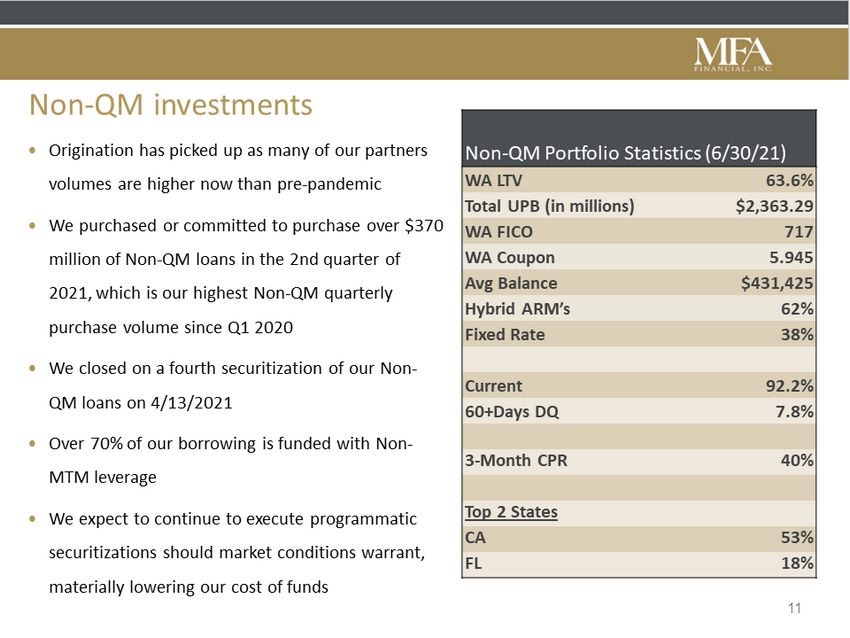

Non - QM investments • Origination has picked up as many of our partners volumes are higher now than pre - pandemic • We purchased or committed to purchase over $370 million of Non - QM loans in the 2nd quarter of 2021, which is our highest Non - QM quarterly purchase volume since Q1 2020 • We closed on a fourth securitization of our Non - QM loans on 4/13/2021 • Over 70% of our borrowing is funded with Non - MTM leverage • We expect to continue to execute programmatic securitizations should market conditions warrant, materially lowering our cost of funds Non - QM Portfolio Statistics (6/30/21) WA LTV 63.6% Total UPB (in millions) $2,363.29 WA FICO 717 WA Coupon 5.945 Avg Balance $431,425 Hybrid ARM’s 62% Fixed Rate 38% Current 92.2% 60+Days DQ 7.8% 3 - Month CPR 40% Top 2 States CA 53% FL 18% 11

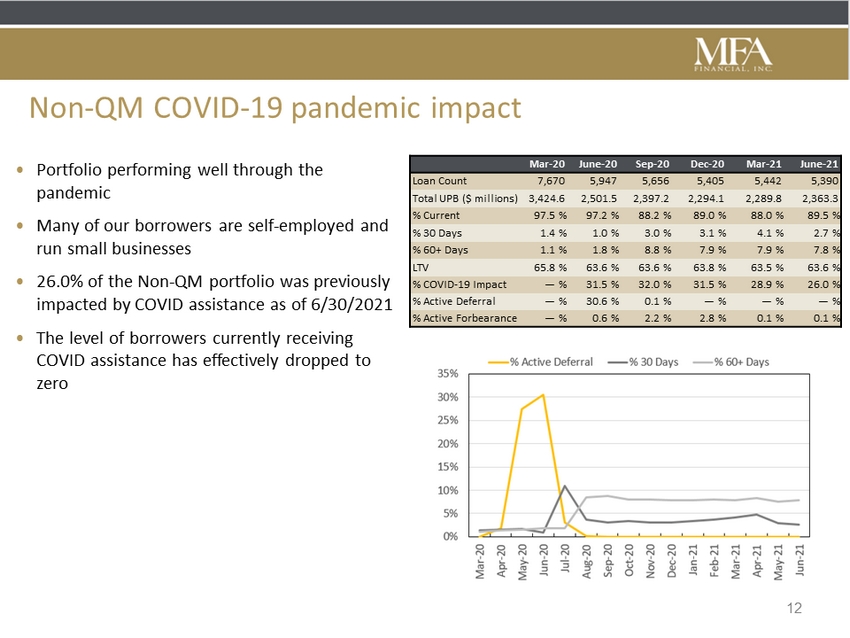

Non - QM COVID - 19 pandemic impact • Portfolio performing well through the pandemic • Many of our borrowers are self - employed and run small businesses • 26.0% of the Non - QM portfolio was previously impacted by COVID assistance as of 6/30/2021 • The level of borrowers currently receiving COVID assistance has effectively dropped to zero Mar - 20 June - 20 Sep - 20 Dec - 20 Mar - 21 June - 21 Loan Count 7,670 5,947 5,656 5,405 5,442 5,390 Total UPB ($ millions) 3,424.6 2,501.5 2,397.2 2,294.1 2,289.8 2,363.3 % Current 97.5 % 97.2 % 88.2 % 89.0 % 88.0 % 89.5 % % 30 Days 1.4 % 1.0 % 3.0 % 3.1 % 4.1 % 2.7 % % 60+ Days 1.1 % 1.8 % 8.8 % 7.9 % 7.9 % 7.8 % LTV 65.8 % 63.6 % 63.6 % 63.8 % 63.5 % 63.6 % % COVID - 19 Impact — % 31.5 % 32.0 % 31.5 % 28.9 % 26.0 % % Active Deferral — % 30.6 % 0.1 % — % — % — % % Active Forbearance — % 0.6 % 2.2 % 2.8 % 0.1 % 0.1 % 12

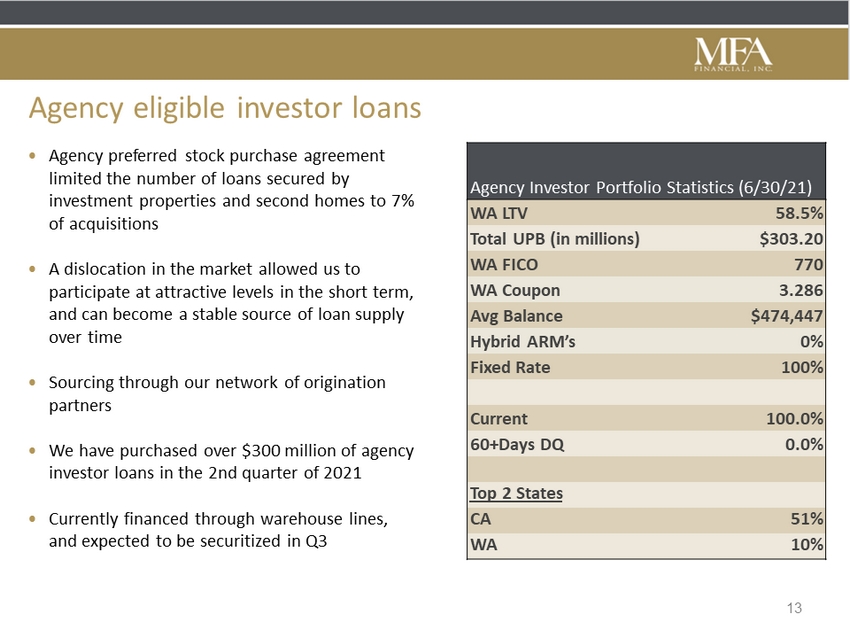

Agency eligible investor loans • Agency preferred stock purchase agreement limited the number of loans secured by investment properties and second homes to 7% of acquisitions • A dislocation in the market allowed us to participate at attractive levels in the short term, and can become a stable source of loan supply over time • Sourcing through our network of origination partners • We have purchased over $300 million of agency investor loans in the 2nd quarter of 2021 • Currently financed through warehouse lines, and expected to be securitized in Q3 13 Agency Investor Portfolio Statistics (6/30/21) WA LTV 58.5% Total UPB (in millions) $303.20 WA FICO 770 WA Coupon 3.286 Avg Balance $474,447 Hybrid ARM’s 0% Fixed Rate 100% Current 100.0% 60+Days DQ 0.0% Top 2 States CA 51% WA 10%

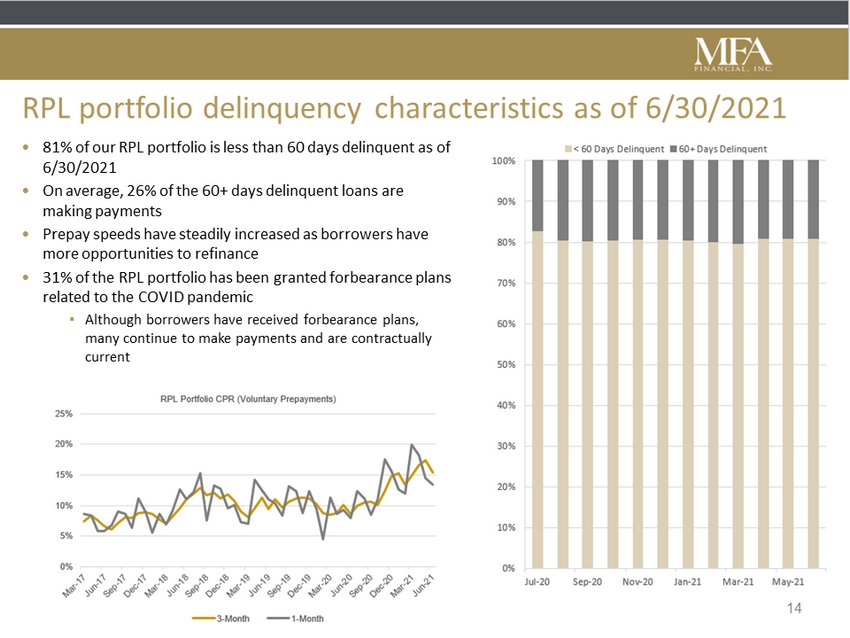

RPL portfolio delinquency characteristics as of 6/30/2021 • 81% of our RPL portfolio is less than 60 days delinquent as of 6/30/2021 • On average, 26% of the 60+ days delinquent loans are making payments • Prepay speeds have steadily increased as borrowers have more opportunities to refinance • 31% of the RPL portfolio has been granted forbearance plans related to the COVID pandemic ▪ Although borrowers have received forbearance plans, many continue to make payments and are contractually current 14

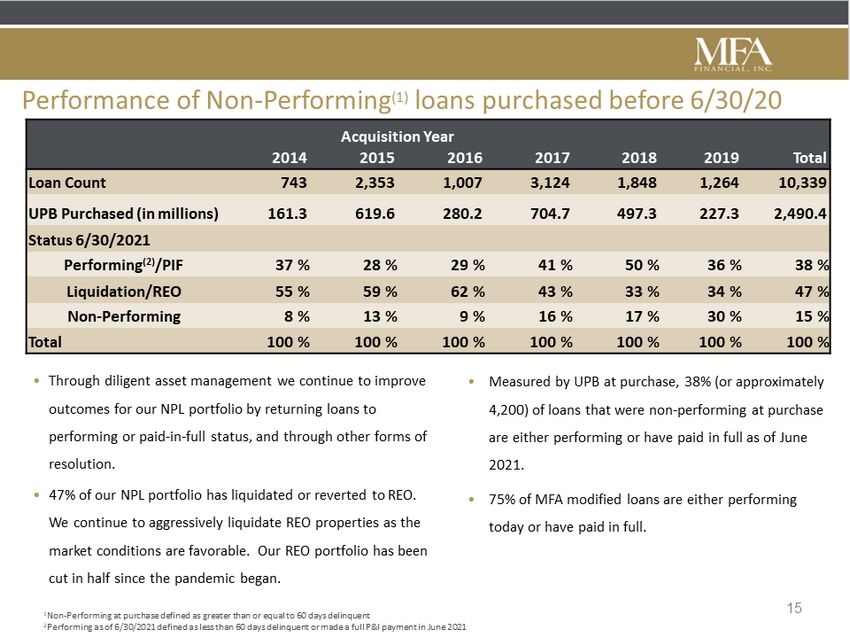

• Measured by UPB at purchase, 38% (or approximately 4,200) of loans that were non - performing at purchase are either performing or have paid in full as of June 2021. • 75% of MFA modified loans are either performing today or have paid in full. Performance of Non - Performing (1) loans purchased before 6/30/20 Acquisition Year 2014 2015 2016 2017 2018 2019 Total Loan Count 743 2,353 1,007 3,124 1,848 1,264 10,339 UPB Purchased (in millions) 161.3 619.6 280.2 704.7 497.3 227.3 2,490.4 Status 6/30/2021 Performing (2) /PIF 37 % 28 % 29 % 41 % 50 % 36 % 38 % Liquidation/REO 55 % 59 % 62 % 43 % 33 % 34 % 47 % Non - Performing 8 % 13 % 9 % 16 % 17 % 30 % 15 % Total 100 % 100 % 100 % 100 % 100 % 100 % 100 % 1 Non - Performing at purchase defined as greater than or equal to 60 days delinquent 2 Performing as of 6/30/2021 defined as less than 60 days delinquent or made a full P&I payment in June 2021 • Through diligent asset management we continue to improve outcomes for our NPL portfolio by returning loans to performing or paid - in - full status, and through other forms of resolution. • 47% of our NPL portfolio has liquidated or reverted to REO. We continue to aggressively liquidate REO properties as the market conditions are favorable. Our REO portfolio has been cut in half since the pandemic began. 15

Business purpose loans – Lima One acquisition • We completed the previously announced acquisition of Lima One on July 1, 2021 • Lima One is a leading nationwide originator and servicer of BPLs with a long relationship with MFA • Lima One has originated in excess of $3 billion of BPLs since inception. Expected to consistently generate in excess of $1 billion of BPLs annually with a clear path to grow meaningfully beyond that • At closing we acquired all of Lima One ’s operating platform and servicing assets, as well as approximately $152 million of loans on balance sheet ▪ Approximately $88 million of Fix and Flip loans ▪ Approximately $64 million in Single Family Rental loans • Integration has been smooth and initiatives to improve financing of Lima One’s operations and on balance sheet assets are progressing well: ▪ Refinancing of expensive BPL securitization and subordinated debt Lima One issued in 2020 ▪ Utilize MFA’s balance sheet and reputation to substantially improve warehouse financing of Lima One’s BPL assets 16

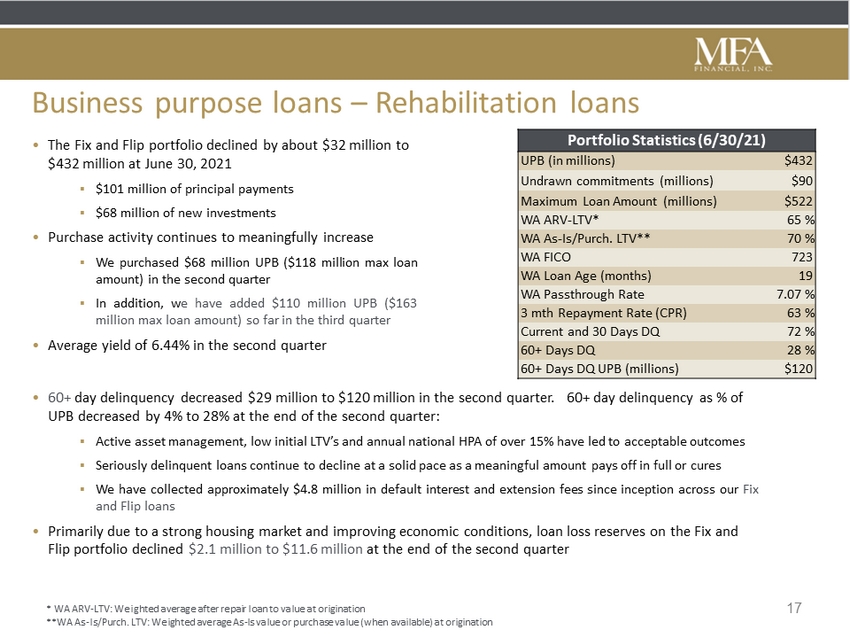

Business purpose loans – Rehabilitation loans • The Fix and Flip portfolio declined by about $32 million to $432 million at June 30, 2021 ▪ $ 101 million of principal payments ▪ $ 68 million of new investments • Purchase activity continues to meaningfully increase ▪ We purchased $ 68 million UPB ( $ 118 million max loan amount) in the second quarter ▪ In addition, w e have added $ 110 million UPB ( $ 163 million max loan amount) so far in the third quarter • Average yield of 6.44% in the second quarter Portfolio Statistics (6/30/21) UPB (in millions) $432 Undrawn commitments (millions) $90 Maximum Loan Amount (millions) $522 WA ARV - LTV* 65 % WA As - Is/Purch. LTV** 70 % WA FICO 723 WA Loan Age (months) 19 WA Passthrough Rate 7.07 % 3 mth Repayment Rate (CPR) 63 % Current and 30 Days DQ 72 % 60+ Days DQ 28 % 60+ Days DQ UPB (millions) $120 * WA ARV - LTV: Weighted average after repair loan to value at origination **WA As - Is/Purch. LTV: Weighted average As - Is value or purchase value (when available) at origination 17 • 60+ day delinquency decreased $29 million to $120 million in the second quarter. 60+ day delinquency as % of UPB decreased by 4% to 28% at the end of the second quarter: ▪ Active asset management, low initial LTV’s and annual national HPA of over 15 % have led to acceptable outcomes ▪ Seriously delinquent loans continue to decline at a solid pace as a meaningful amount pays off in full or cures ▪ We have collected approximately $ 4 . 8 million in default interest and extension fees since inception across our Fix and Flip loans • Primarily due to a strong housing market and improving economic conditions, loan loss reserves on the Fix and Flip portfolio declined $2.1 million to $11.6 million at the end of the second quarter

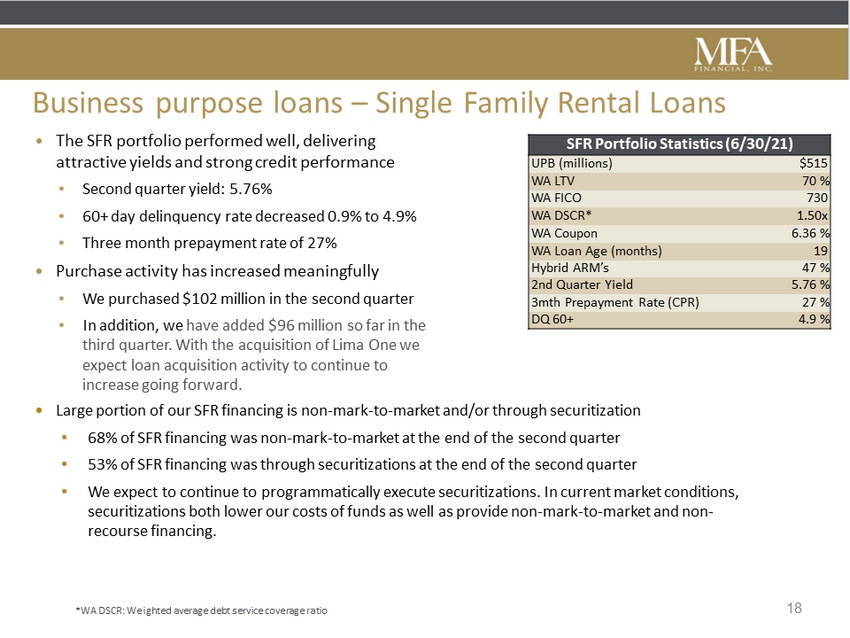

Business purpose loans – Single Family Rental Loans • The SFR portfolio performed well, delivering attractive yields and strong credit performance ▪ Second quarter yield: 5.76% ▪ 60+ day delinquency rate decreased 0.9% to 4.9% ▪ Three month prepayment rate of 27% • Purchase activity has increased meaningfully ▪ We purchased $102 million in the second quarter ▪ In addition, we have added $96 million so far in the third quarter. With the acquisition of Lima One we expect loan acquisition activity to continue to increase going forward. SFR Portfolio Statistics (6/30/21) UPB (millions) $515 WA LTV 70 % WA FICO 730 WA DSCR* 1.50x WA Coupon 6.36 % WA Loan Age (months) 19 Hybrid ARM’s 47 % 2nd Quarter Yield 5.76 % 3mth Prepayment Rate (CPR) 27 % DQ 60+ 4.9 % *WA DSCR: Weighted average debt service coverage ratio 18 • Large portion of our SFR financing is non - mark - to - market and/or through securitization ▪ 68% of SFR financing was non - mark - to - market at the end of the second quarter ▪ 53% of SFR financing was through securitizations at the end of the second quarter ▪ We expect to continue to programmatically execute securitizations. In current market conditions, securitizations both lower our costs of funds as well as provide non - mark - to - market and non - recourse financing.

Summary • Very solid second quarter 2021 results in a difficult quarter for mortgage investors ▪ Stable book value ▪ Continued improvement in net interest income ▪ Portfolio acquisitions exceeded runoff for first time since COVID onset • Successful execution of securitization transactions has generated substantial liquidity and positively impacted our cost of funds . Securitized debt has the added benefit of being non - recourse term financing without mark - to - market collateral maintenance • Acquisition of Lima One is a transformative event that we believe will enhance our ability to purchase and service high quality business purpose loans and be accretive to earnings • Strong housing and economic fundamentals have positive implications for mortgage credit and the performance of our portfolio 19

Additional Information

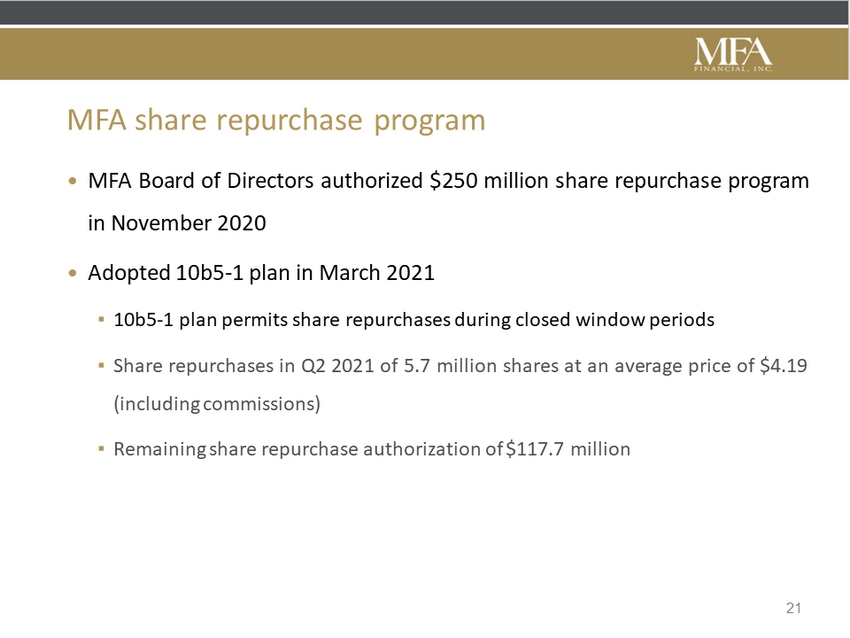

• MFA Board of Directors authorized $ 250 million share repurchase program in November 2020 • Adopted 10 b 5 - 1 plan in March 2021 ▪ 10 b 5 - 1 plan permits share repurchases during closed window periods ▪ Share repurchases in Q 2 2021 of 5 . 7 million shares at an average price of $ 4 . 19 (including commissions) ▪ Remaining share repurchase authorization of $ 117 . 7 million 21 MFA share repurchase program

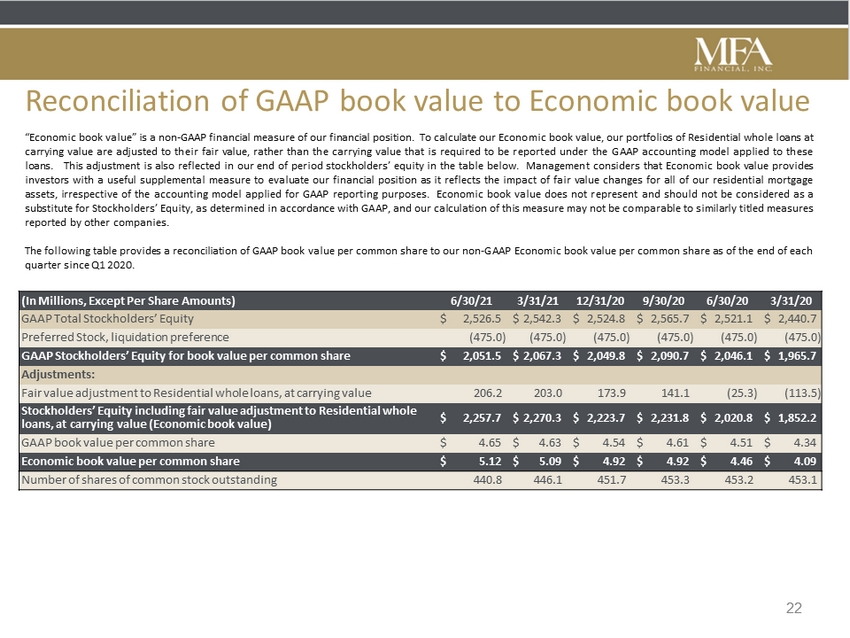

22 Reconciliation of GAAP book value to Economic book value “Economic book value” is a non - GAAP financial measure of our financial position . To calculate our Economic book value, our portfolios of Residential whole loans at carrying value are adjusted to their fair value, rather than the carrying value that is required to be reported under the GAAP accounting model applied to these loans . This adjustment is also reflected in our end of period stockholders’ equity in the table below . Management considers that Economic book value provides investors with a useful supplemental measure to evaluate our financial position as it reflects the impact of fair value changes for all of our residential mortgage assets, irrespective of the accounting model applied for GAAP reporting purposes . Economic book value does not represent and should not be considered as a substitute for Stockholders’ Equity, as determined in accordance with GAAP, and our calculation of this measure may not be comparable to similarly titled measures reported by other companies . The following table provides a reconciliation of GAAP book value per common share to our non - GAAP Economic book value per common share as of the end of each quarter since Q 1 2020 . (In Millions, Except Per Share Amounts) 6/30/21 3/31/21 12/31/20 9/30/20 6/30/20 3/31/20 GAAP Total Stockholders’ Equity $ 2,526.5 $ 2,542.3 $ 2,524.8 $ 2,565.7 $ 2,521.1 $ 2,440.7 Preferred Stock, liquidation preference (475.0 ) (475.0 ) (475.0 ) (475.0 ) (475.0 ) (475.0 ) GAAP Stockholders’ Equity for book value per common share $ 2,051.5 $ 2,067.3 $ 2,049.8 $ 2,090.7 $ 2,046.1 $ 1,965.7 Adjustments: Fair value adjustment to Residential whole loans, at carrying value 206.2 203.0 173.9 141.1 (25.3 ) (113.5 ) Stockholders’ Equity including fair value adjustment to Residential whole loans, at carrying value (Economic book value) $ 2,257.7 $ 2,270.3 $ 2,223.7 $ 2,231.8 $ 2,020.8 $ 1,852.2 GAAP book value per common share $ 4.65 $ 4.63 $ 4.54 $ 4.61 $ 4.51 $ 4.34 Economic book value per common share $ 5.12 $ 5.09 $ 4.92 $ 4.92 $ 4.46 $ 4.09 Number of shares of common stock outstanding 440.8 446.1 451.7 453.3 453.2 453.1

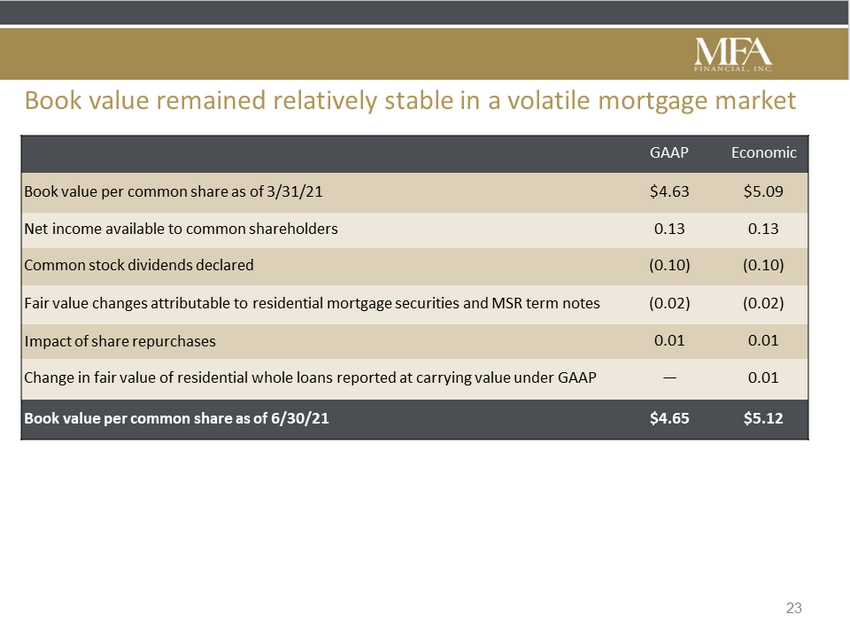

23 GAAP Economic Book value per common share as of 3/31/21 $4.63 $5.09 Net income available to common shareholders 0.13 0.13 Common stock dividends declared (0.10) (0.10) Fair value changes attributable to residential mortgage securities and MSR term notes (0.02) (0.02) Impact of share repurchases 0.01 0.01 Change in fair value of residential whole loans reported at carrying value under GAAP — 0.01 Book value per common share as of 6/30/21 $4.65 $5.12 Book value remained relatively stable in a volatile mortgage market

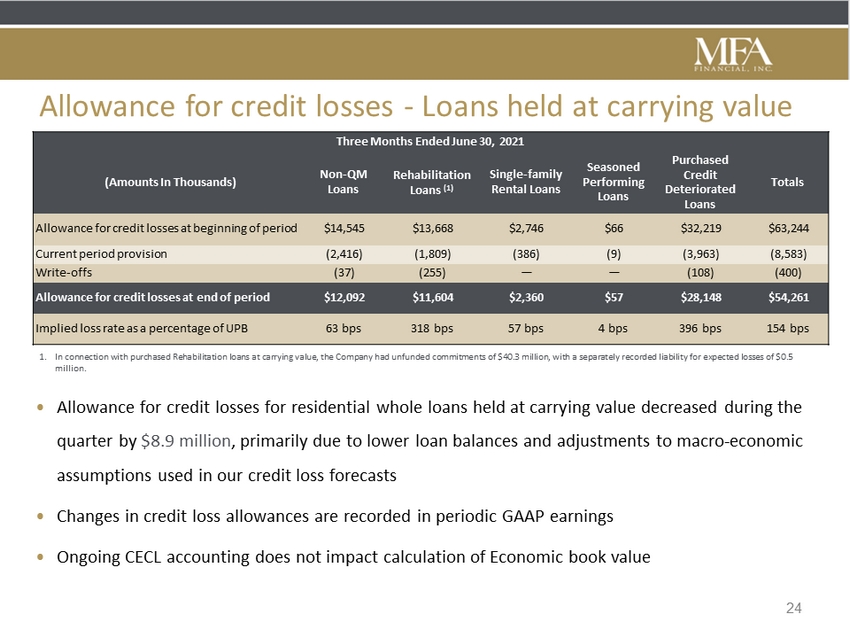

Allowance for credit losses - Loans held at carrying value • Allowance for credit losses for residential whole loans held at carrying value decreased during the quarter by $8.9 million , primarily due to lower loan balances and adjustments to macro - economic assumptions used in our credit loss forecasts • Changes in credit loss allowances are recorded in periodic GAAP earnings • Ongoing CECL accounting does not impact calculation of Economic book value 24 Three Months Ended June 30, 2021 (Amounts In Thousands) Non - QM Loans Rehabilitation Loans (1) Single - family Rental Loans Seasoned Performing Loans Purchased Credit Deteriorated Loans Totals Allowance for credit losses at beginning of period $14,545 $13,668 $2,746 $66 $32,219 $63,244 Current period provision (2,416) (1,809) (386) (9) (3,963) (8,583) Write - offs (37) (255) — — (108) (400) Allowance for credit losses at end of period $12,092 $11,604 $2,360 $57 $28,148 $54,261 Implied loss rate as a percentage of UPB 63 bps 318 bps 57 bps 4 bps 396 bps 154 bps 1. In connection with purchased Rehabilitation loans at carrying value, the Company had unfunded commitments of $ 40 . 3 million, with a separately recorded liability for expected losses of $ 0 . 5 million .