EXHIBIT 99.2

Published on November 6, 2024

Exhibit 99.2

Company Update THIRD QUARTER 2024

2 Q3 202 2 Financial Snapshot Forward - looking statements When used in this presentation or other written or oral communications, statements that are not historical in nature, including those containing words such as “will,” “believe,” “expect,” “anticipate,” “estimate,” “plan,” “continue,” “intend,” “should,” “could,” “would,” “may,” the negative of these words or similar expressions, are intended to identify “forward - looking statements” within the meaning of Section 27 A of the Securities Act of 1933 , as amended, and Section 21 E of the Securities Exchange Act of 1934 , as amended, and, as such, may involve known and unknown risks, uncertainties and assumptions . These forward - looking statements include information about possible or assumed future results with respect to MFA’s business, financial condition, liquidity, results of operations, plans and objectives . Among the important factors that could cause our actual results to differ materially from those projected in any forward - looking statements that we make are : general economic developments and trends and the performance of the housing, real estate, mortgage finance, broader financial markets ; inflation, increases in interest rates and changes in the market (i . e . , fair) value of MFA’s residential whole loans, MBS, securitized debt and other assets, as well as changes in the value of MFA’s liabilities accounted for at fair value through earnings ; the effectiveness of hedging transactions ; changes in the prepayment rates on residential mortgage assets, an increase of which could result in a reduction of the yield on certain investments in its portfolio and could require MFA to reinvest the proceeds received by it as a result of such prepayments in investments with lower coupons, while a decrease in which could result in an increase in the interest rate duration of certain investments in MFA’s portfolio making their valuation more sensitive to changes in interest rates and could result in lower forecasted cash flows ; credit risks underlying MFA’s assets, including changes in the default rates and management’s assumptions regarding default rates and loss severities on the mortgage loans in MFA’s residential whole loan portfolio ; MFA’s ability to borrow to finance its assets and the terms, including the cost, maturity and other terms, of any such borrowings ; implementation of or changes in government regulations or programs affecting MFA’s business ; MFA’s estimates regarding taxable income, the actual amount of which is dependent on a number of factors, including, but not limited to, changes in the amount of interest income and financing costs, the method elected by MFA to accrete the market discount on residential whole loans and the extent of prepayments, realized losses and changes in the composition of MFA’s residential whole loan portfolios that may occur during the applicable tax period, including gain or loss on any MBS disposals or whole loan modifications, foreclosures and liquidations ; the timing and amount of distributions to stockholders, which are declared and paid at the discretion of MFA’s Board of Directors and will depend on, among other things, MFA’s taxable income, its financial results and overall financial condition and liquidity, maintenance of its REIT qualification and such other factors as MFA’s Board of Directors deems relevant ; MFA’s ability to maintain its qualification as a REIT for federal income tax purposes ; MFA’s ability to maintain its exemption from registration under the Investment Company Act of 1940 , as amended (or the “Investment Company Act”), including statements regarding the concept release issued by the Securities and Exchange Commission (“SEC”) relating to interpretive issues under the Investment Company Act with respect to the status under the Investment Company Act of certain companies that are engaged in the business of acquiring mortgages and mortgage - related interests ; MFA’s ability to continue growing its residential whole loan portfolio, which is dependent on, among other things, the supply of loans offered for sale in the market ; targeted or expected returns on our investments in recently - originated mortgage loans, the performance of which is, similar to our other mortgage loan investments, subject to, among other things, differences in prepayment risk, credit risk and financing costs associated with such investments ; risks associated with the ongoing operation of Lima One Holdings, LLC (including, without limitation, industry competition, unanticipated expenditures relating to or liabilities arising from its operation (including, among other things, a failure to realize management’s assumptions regarding expected growth in business purpose loan (BPL) origination volumes and credit risks underlying BPLs, including changes in the default rates and management’s assumptions regarding default rates and loss severities on the BPLs originated by Lima One) ; expected returns on MFA’s investments in nonperforming residential whole loans (“NPLs”), which are affected by, among other things, the length of time required to foreclose upon, sell, liquidate or otherwise reach a resolution of the property underlying the NPL, home price values, amounts advanced to carry the asset (e . g . , taxes, insurance, maintenance expenses, etc . on the underlying property) and the amount ultimately realized upon resolution of the asset ; risks associated with our investments in MSR - related assets, including servicing, regulatory and economic risks ; risks associated with our investments in loan originators ; risks associated with investing in real estate assets generally, including changes in business conditions and the general economy ; and other risks, uncertainties and factors, including those described in the annual, quarterly and current reports that we file with the SEC . These forward - looking statements are based on beliefs, assumptions and expectations of MFA’s future performance, taking into account information currently available . Readers and listeners are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date on which they are made . New risks and uncertainties arise over time and it is not possible to predict those events or how they may affect MFA . Except as required by law, MFA is not obligated to, and does not intend to, update or revise any forward - looking statements, whether as a result of new information, future events or otherwise .

3 v MFA at a glance 3 $1.9B Total equity 1998 Listed on NYSE in Leading hybrid mortgage REIT with extensive experience in managing residential mortgage assets through economic cycles $11.2B Total assets NYSE: MFA $4.8B Common dividends as of Sept. 30, 2024 as of Sept. 30, 2024 paid since IPO See page 27 for endnotes Dividend yield 11.5% as of Nov. 1, 2024 Loans acquired 1 $24B since 2014

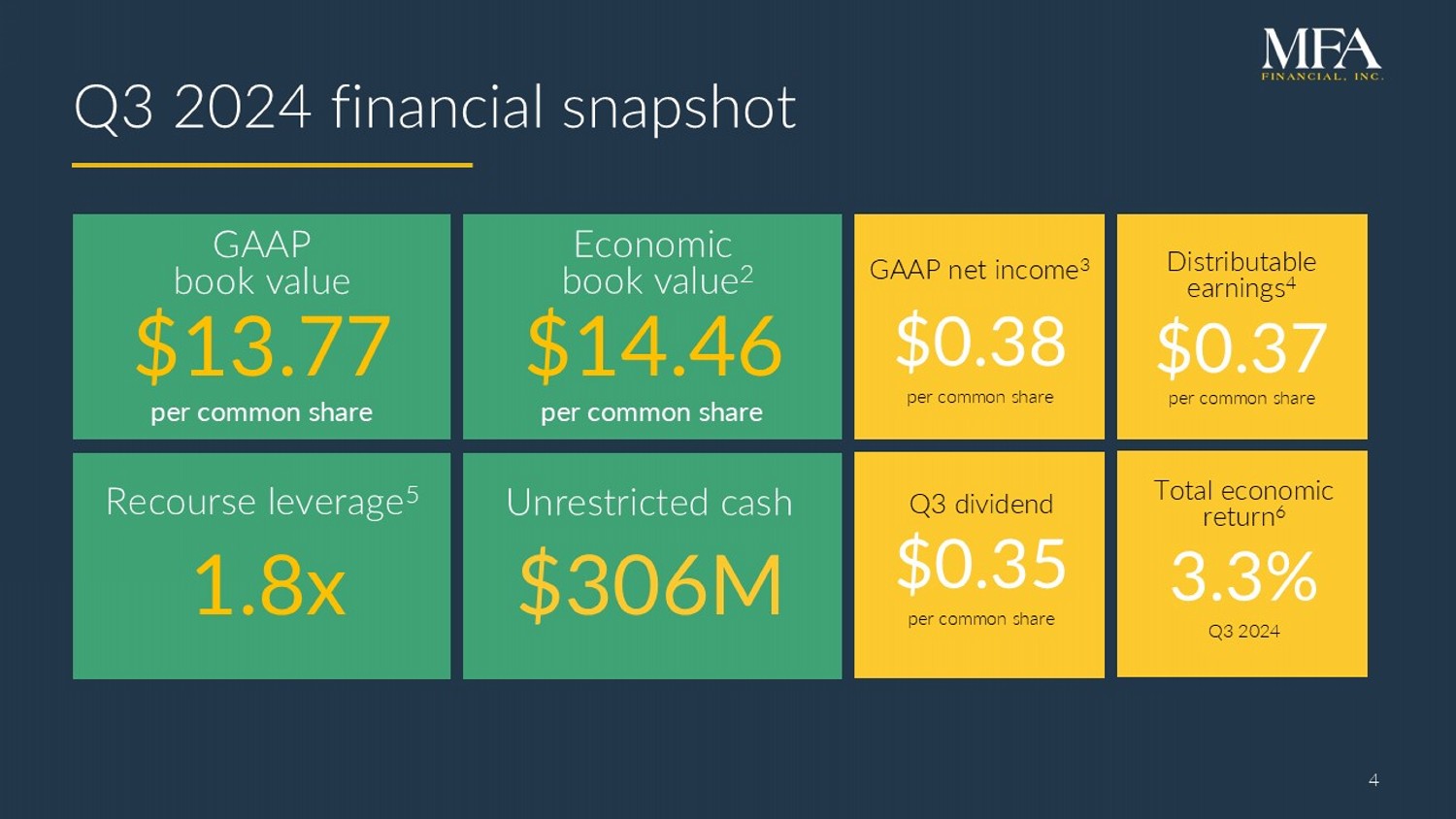

4 Q 3 202 4 financial snapshot $13.77 $14.46 GAAP net income 3 $0.38 per common share Distributable earnings 4 $0.37 per common share GAAP book value Economic book value 2 per common share per common share $306M Unrestricted cash 1.8x Recourse leverage 5 4 Q3 dividend $0.35 per common share Total economic return 6 3.3% Q3 2024

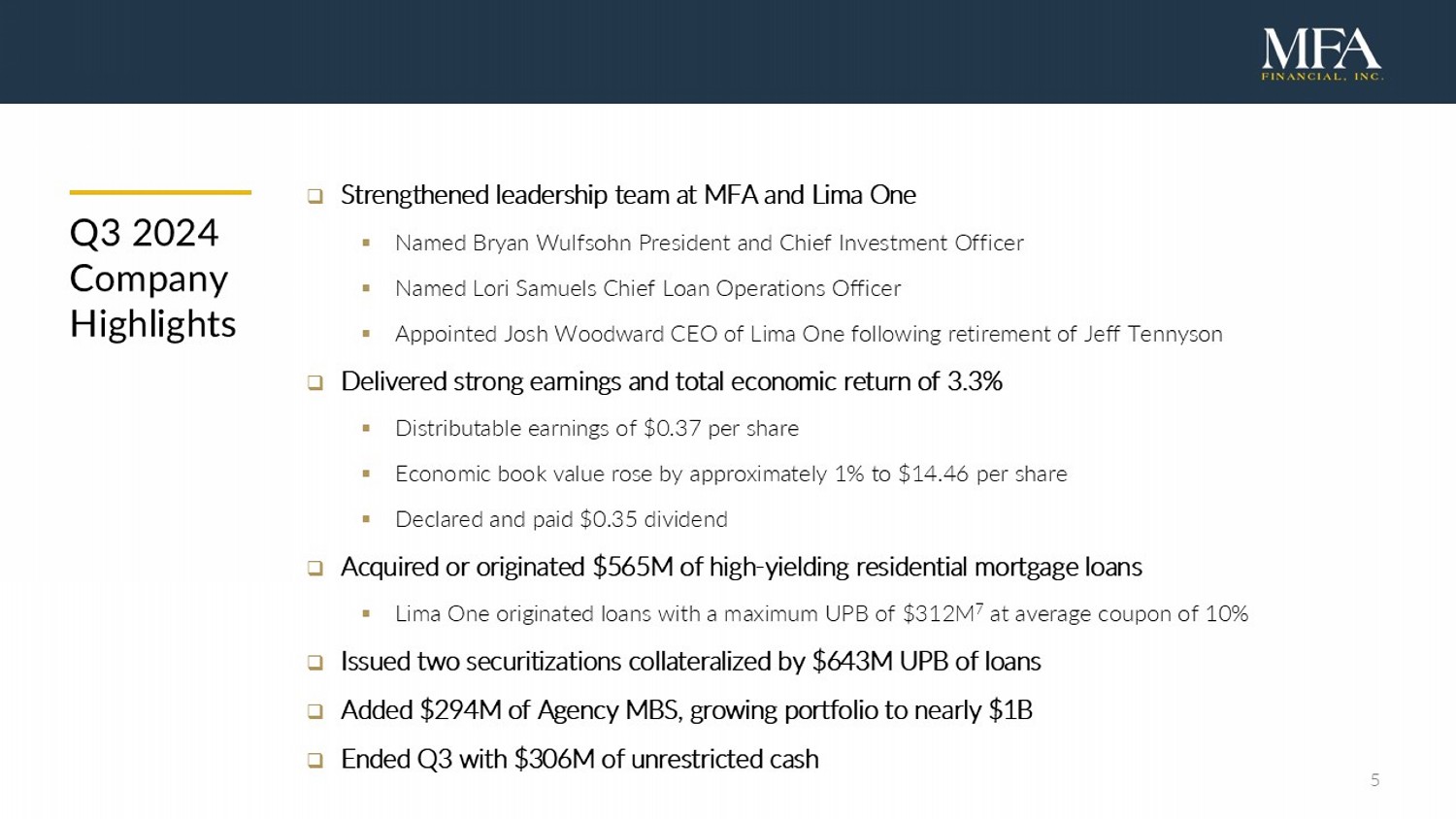

5 Q3 2024 Company Highlights □ Strengthened leadership team at MFA and Lima One ▪ Named Bryan Wulfsohn President and Chief Investment Officer ▪ Named Lori Samuels Chief Loan Operations Officer ▪ Appointed Josh Woodward CEO of Lima One following retirement of Jeff Tennyson □ Delivered strong earnings and total economic return of 3.3% ▪ Distributable earnings of $0.37 per share ▪ Economic book value rose by approximately 1% to $14.46 per share ▪ Declared and paid $0.35 dividend □ Acquired or originated $565M of high - yielding residential mortgage loans ▪ Lima One originated loans with a maximum UPB of $312M 7 at average coupon of 10% □ Issued two securitizations collateralized by $643M UPB of loans □ Added $294M of Agency MBS, growing portfolio to nearly $1B □ Ended Q3 with $306M of unrestricted cash

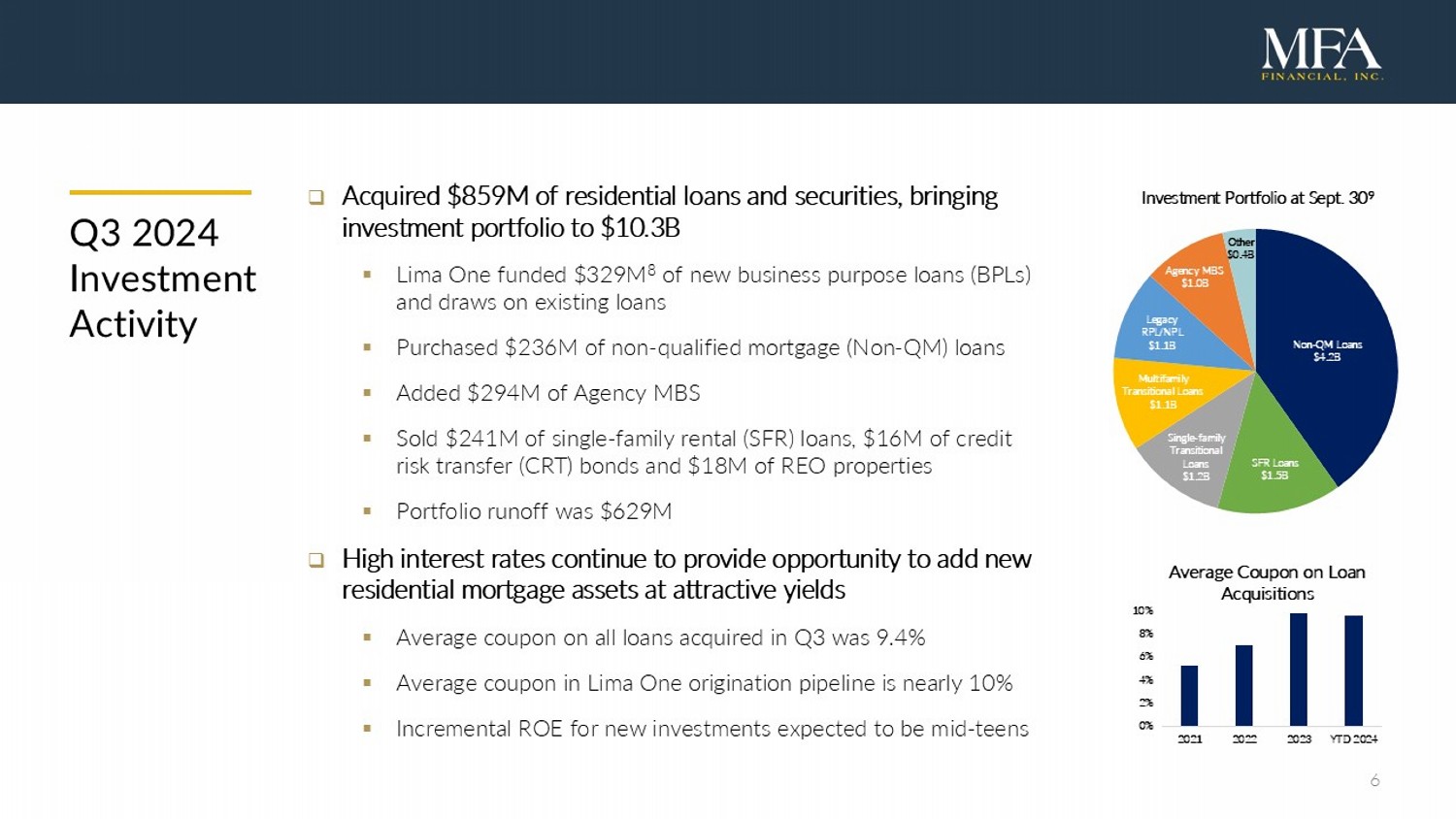

6 □ Acquired $859M of residential loans and securities, bringing investment portfolio to $10.3B ▪ Lima One funded $329M 8 of new business purpose loans (BPLs) and draws on existing loans ▪ Purchased $236M of non - qualified mortgage (Non - QM) loans ▪ Added $294M of Agency MBS ▪ Sold $241M of single - family rental (SFR) loans, $16M of credit risk transfer (CRT) bonds and $18M of REO properties ▪ Portfolio runoff was $629M □ High interest rates continue to provide opportunity to add new residential mortgage assets at attractive yields ▪ Average coupon on all loans acquired in Q3 was 9.4% ▪ Average coupon in Lima One origination pipeline is nearly 10% ▪ Incremental ROE for new investments expected to be mid - teens Q3 2024 Investment Activity 0% 2% 4% 6% 8% 10% 2021 2022 2023 YTD 2024 Average Coupon on Loan Acquisitions Non - QM Loans $4.2B SFR Loans $1.5B Single - family Transitional Loans $1.2B Multifamily Transitional Loans $1.1B Legacy RPL/NPL $1.1B Agency MBS $1.0B Other $0.4B Investment Portfolio at Sept. 30 9

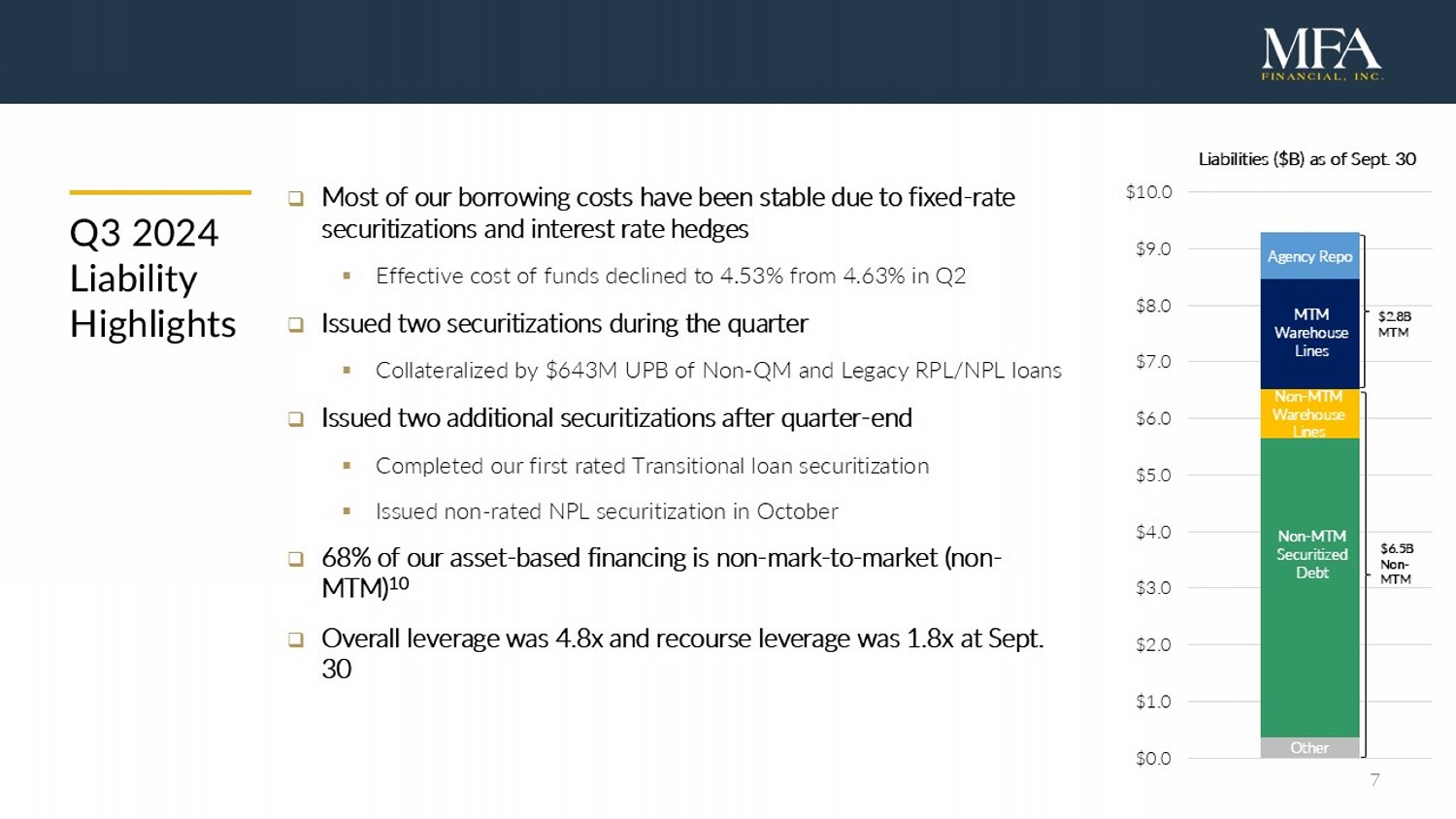

7 Q3 2024 Liability Highlights □ Most of our borrowing costs have been stable due to fixed - rate securitizations and interest rate hedges ▪ Effective cost of funds declined to 4.53% from 4.63% in Q2 □ Issued two securitizations during the quarter ▪ Collateralized by $643M UPB of Non - QM and Legacy RPL/NPL loans □ Issued two additional securitizations after quarter - end ▪ Completed our first rated Transitional loan securitization ▪ Issued non - rated NPL securitization in October □ 68% of our asset - based financing is non - mark - to - market (non - MTM) 10 □ Overall leverage was 4.8x and recourse leverage was 1.8x at Sept. 30 MTM Warehouse Line Non - MTM Warehouse Line Non - MTM Securitized Debt Other $2.8B MTM $6.5B Non - MTM $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 $8.0 $9.0 $10.0 Liabilities ($B) as of Sept. 30 Agency Repo MTM Warehouse Lines Non - MTM Warehouse Lines Non - MTM Securitized Debt Other

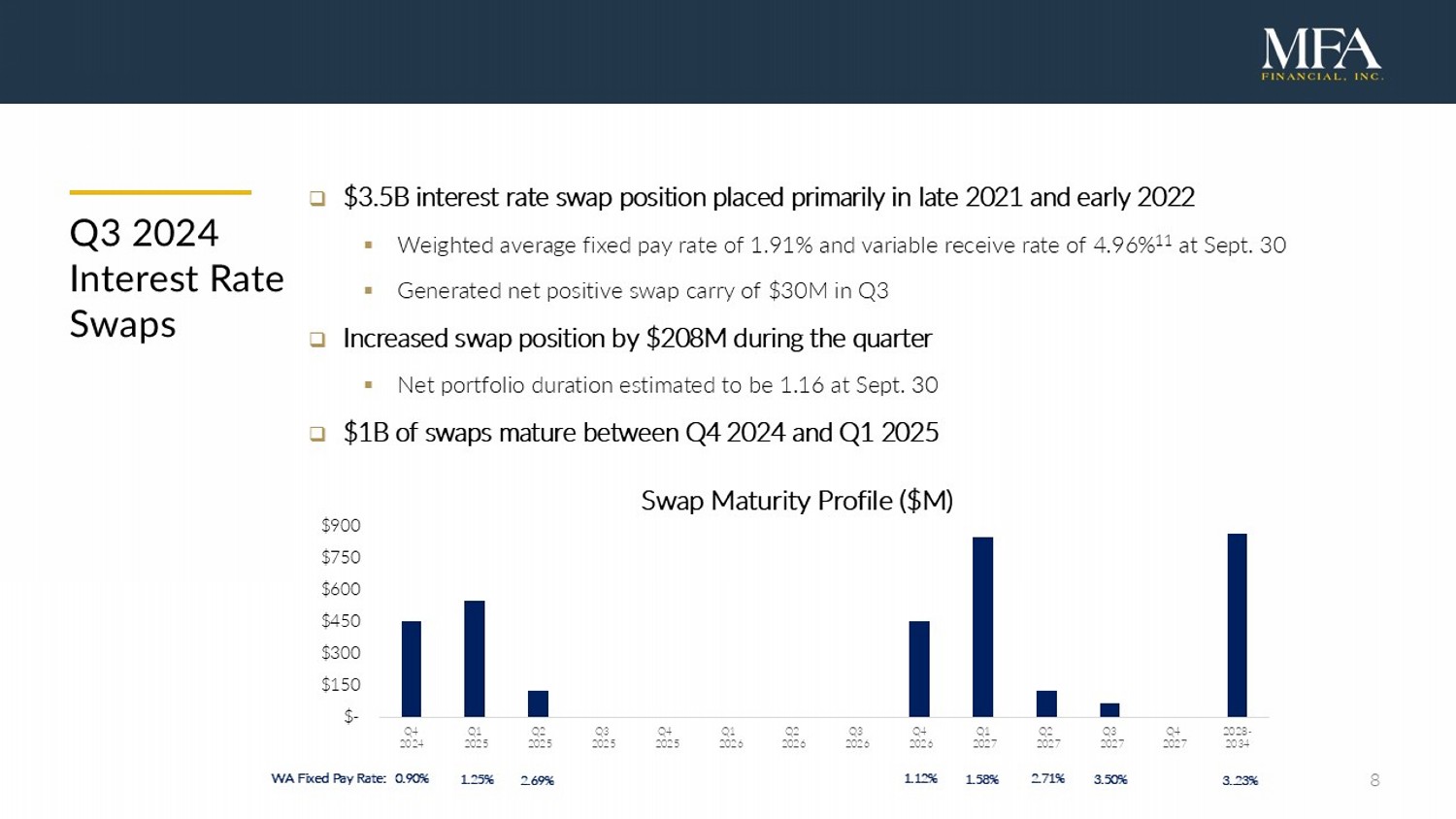

8 Q3 2024 Interest Rate Swaps □ $3.5B interest rate swap position placed primarily in late 2021 and early 2022 ▪ Weighted average fixed pay rate of 1.91% and variable receive rate of 4.96% 11 at Sept. 30 ▪ Generated net positive swap carry of $30M in Q3 □ Increased swap position by $208M during the quarter ▪ Net portfolio duration estimated to be 1.16 at Sept. 30 □ $1B of swaps mature between Q4 2024 and Q1 2025 0.90% 1.25% WA Fixed Pay Rate: 2.69% 1.12% 1.58% 2.71% 3..23% 3.50% $- $150 $300 $450 $600 $750 $900 Q4 2024 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Q2 2026 Q3 2026 Q4 2026 Q1 2027 Q2 2027 Q3 2027 Q4 2027 2028- 2034 Swap Maturity Profile ($M)

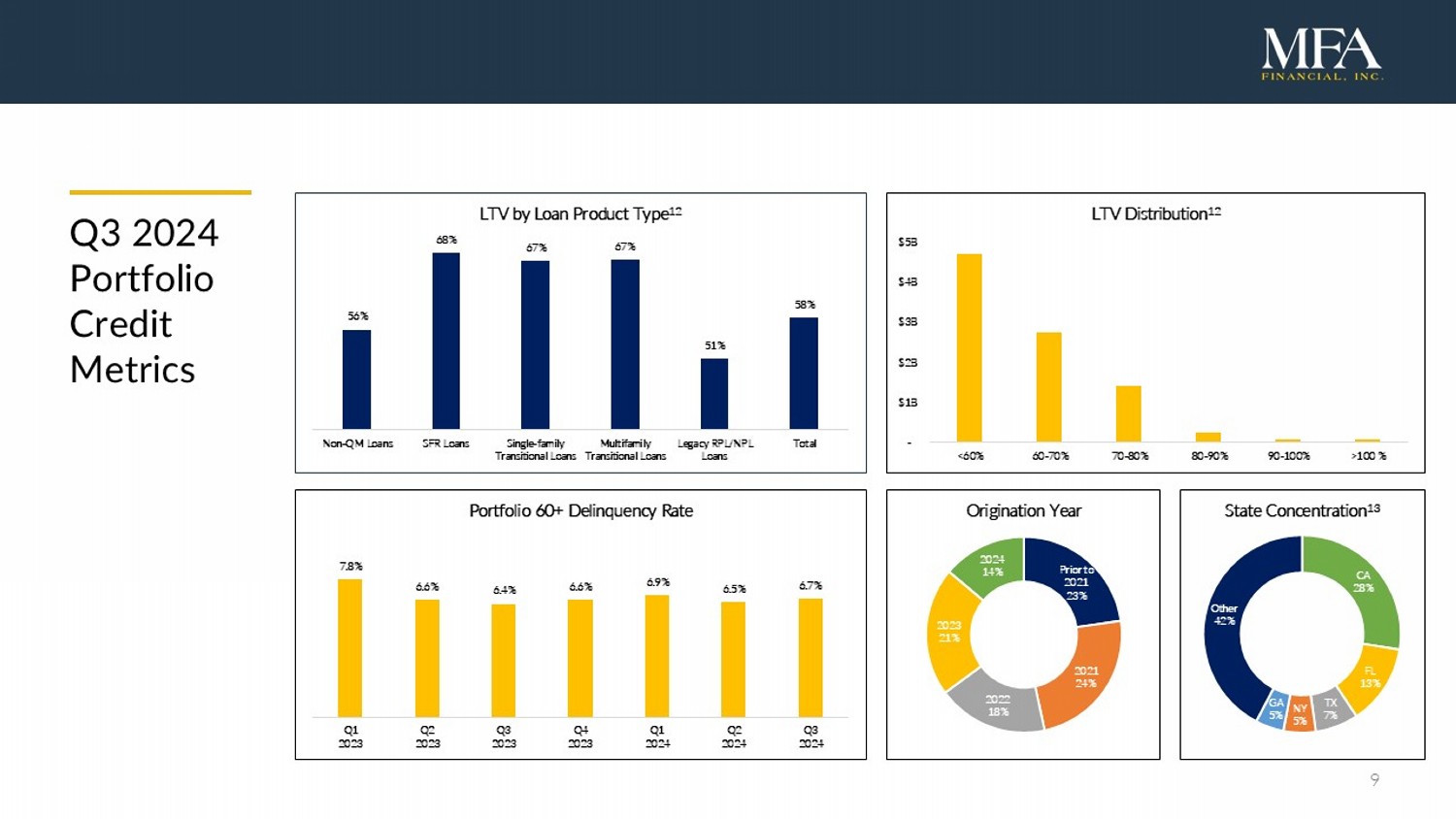

9 Q3 2024 Portfolio Credit Metrics CA 28% FL 13% TX 7% NY 5% GA 5% Other 42% State Concentration 13 56% 68% 67% 67% 51% 58% Non-QM Loans SFR Loans Single-family Transitional Loans Multifamily Transitional Loans Legacy RPL/NPL Loans Total LTV by Loan Product Type 12 - $1B $2B $3B $4B $5B <60% 60-70% 70-80% 80-90% 90-100% >100 % LTV Distribution 12 7.8% 6.6% 6.4% 6.6% 6.9% 6.5% 6.7% Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Portfolio 60+ Delinquency Rate Prior to 2021 23% 2021 24% 2022 18% 2023 21% 2024 14% Origination Year

10 □ Origination volume declined to $312M in Q3 □ Single - family Transitional loan originations totaled $236M ▪ $51M of bridge loans ▪ $83M of rehab (“fix/flip”) loans ▪ $102M of ground - up construction loans □ SFR loan originations were $76M □ Initiated programmatic sales of new origination to 3 rd party investors □ Regular loan sales strengthen Lima One’s franchise value and enhance MFA’s returns □ Sold $77M of newly - originated SFR loans, generating over $3M of gain - on - sale income □ Mortgage banking income totaled $8.9M for the quarter Q3 2024 Lima One Highlights

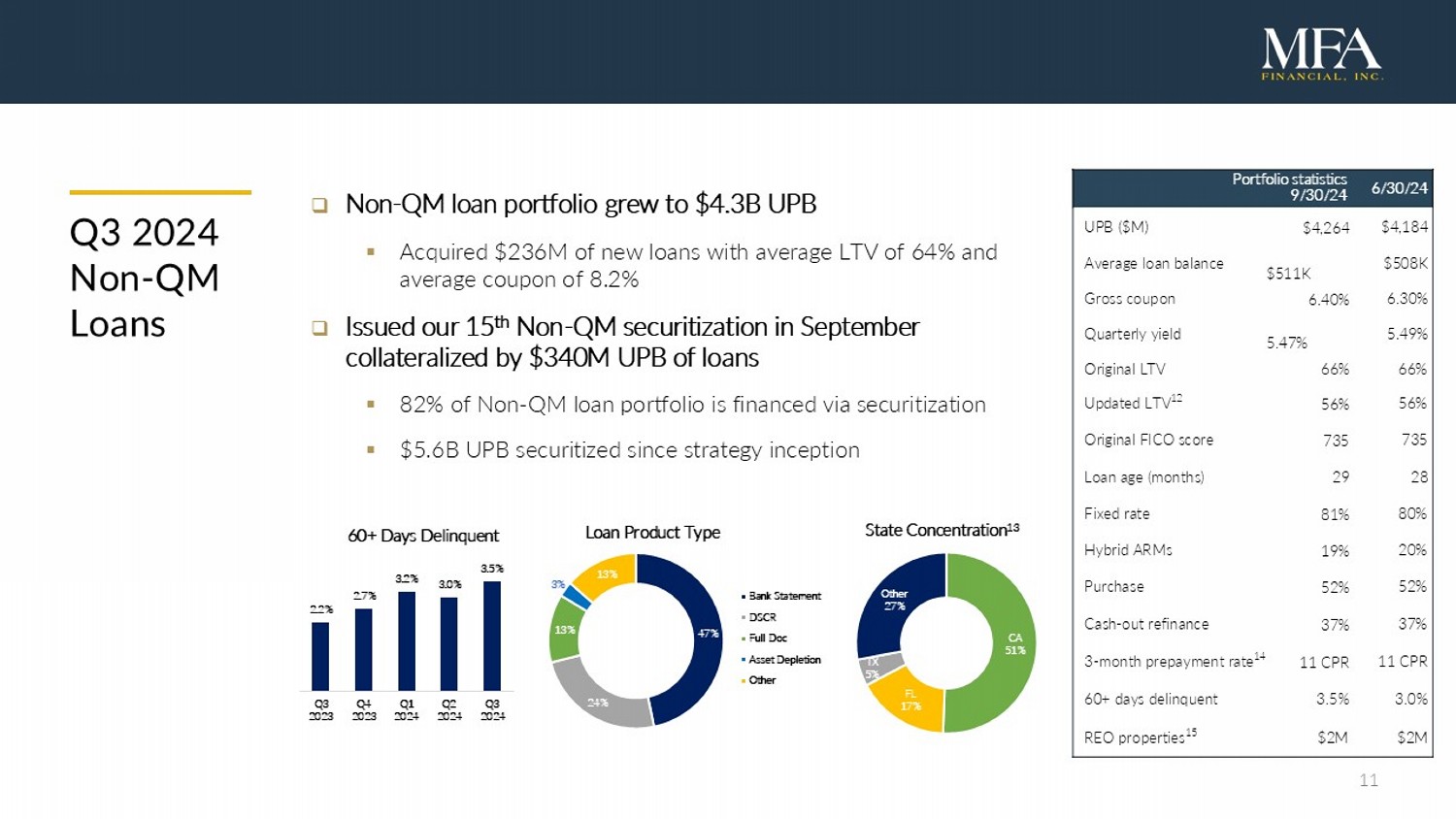

11 Q3 2024 Non - QM Loans □ Non - QM loan portfolio grew to $4.3B UPB ▪ Acquired $236M of new loans with average LTV of 64% and average coupon of 8.2% □ Issued our 15 th Non - QM securitization in September collateralized by $340M UPB of loans ▪ 82% of Non - QM loan portfolio is financed via securitization ▪ $5.6B UPB securitized since strategy inception 6/30/24 P ortfolio s tatistics 9/30/24 $4,184 1 $4,264 UPB ($M) $508K 1 $511K Average loan balance 6.30% 1 6.40% Gross coupon 5.49% 1 5.47% Quarterly yield 66% 1 66% Original LTV 56% 1 56% Updated LTV 12 735 1 735 Original FICO score 28 1 29 Loan age (months) 80% 1 81% Fixed rate 20% 1 19% Hybrid ARMs 52% 1 52% Purchase 37% 1 37% Cash - out refinance 11 CPR 1 11 CPR 3 - month prepayment rate 14 3.0% 1 3.5% 60+ days delinquent $2M 1 $2M REO properties 15 CA 51% FL 17% TX 5% Other 27% State Concentration 13 2.2% 2.7% 3.2% 3.0% 3.5% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 60+ Days Delinquent 47% 24% 13% 3% 13% Loan Product Type Bank Statement DSCR Full Doc Asset Depletion Other

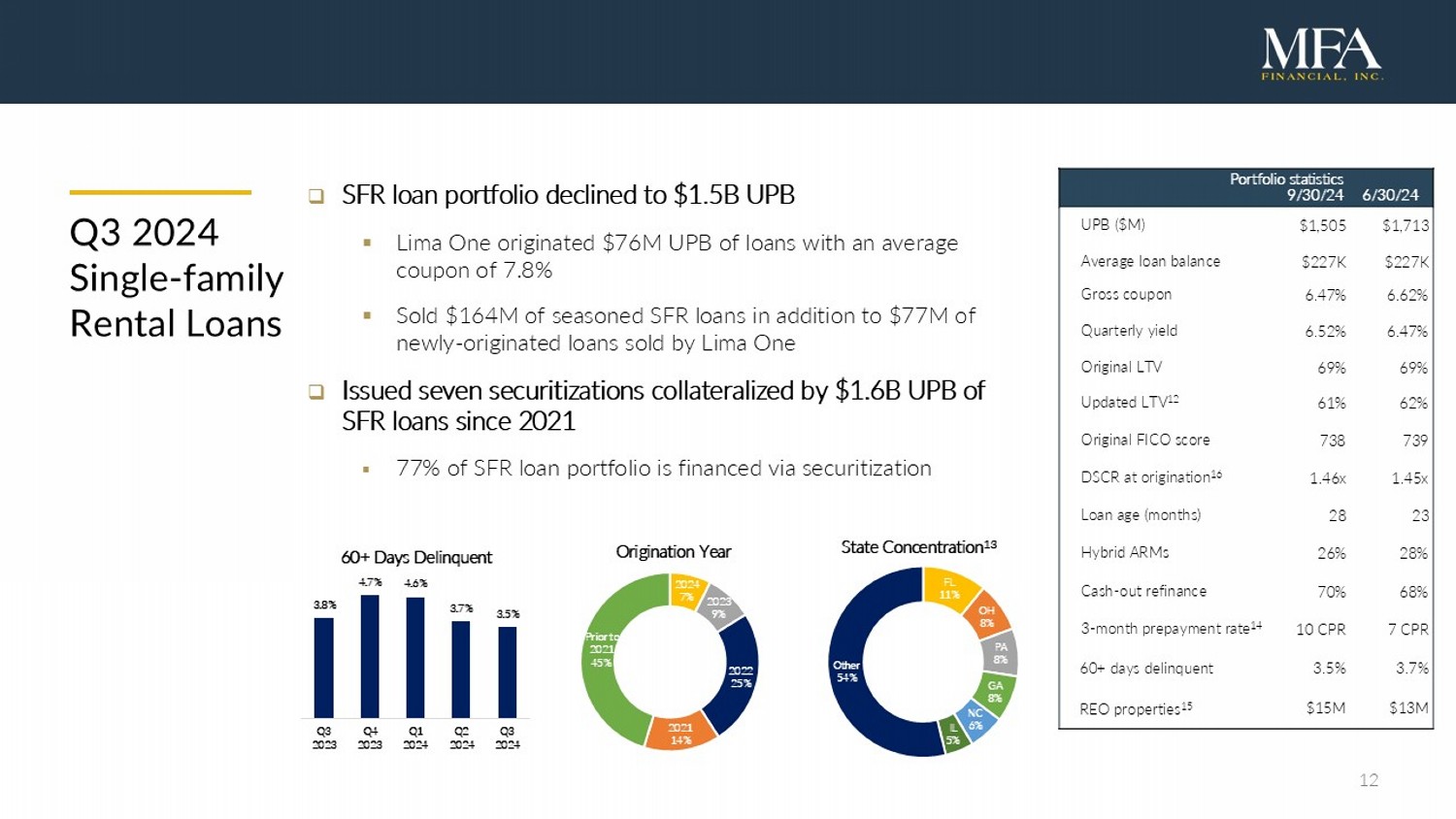

12 6/30/24 P ortfolio s tatistics 9/30/24 $1,713 d $1,505 UPB ($M) $227K d $227K Average loan balance 6.62% d 6.47% Gross coupon 6.47% d 6.52% Quarterly yield 69% d 69% Original LTV 62% d 61% Updated LTV 12 739 d 738 Original FICO score 1.45x d 1.46x DSCR at origination 16 23 d 28 Loan age (months) 28% d 26% Hybrid ARMs 68% d 70% Cash - out refinance 7 CPR d 10 CPR 3 - month prepayment rate 14 3.7% d 3.5% 60+ days delinquent $13M d $15M REO properties 15 Q3 2024 Single - family Rental Loans □ SFR loan portfolio declined to $1.5B UPB ▪ Lima One originated $76M UPB of loans with an average coupon of 7.8% ▪ Sold $164M of seasoned SFR loans in addition to $77M of newly - originated loans sold by Lima One □ Issued seven securitizations collateralized by $1.6B UPB of SFR loans since 2021 ▪ 77% of SFR loan portfolio is financed via securitization FL 11% OH 8% PA 8% GA 8% NC 6% IL 5% Other 54% State Concentration 13 3.8% 4.7% 4.6% 3.7% 3.5% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 60+ Days Delinquent 2024 7% 2023 9% 2022 25% 2021 14% Prior to 2021 45% Origination Year

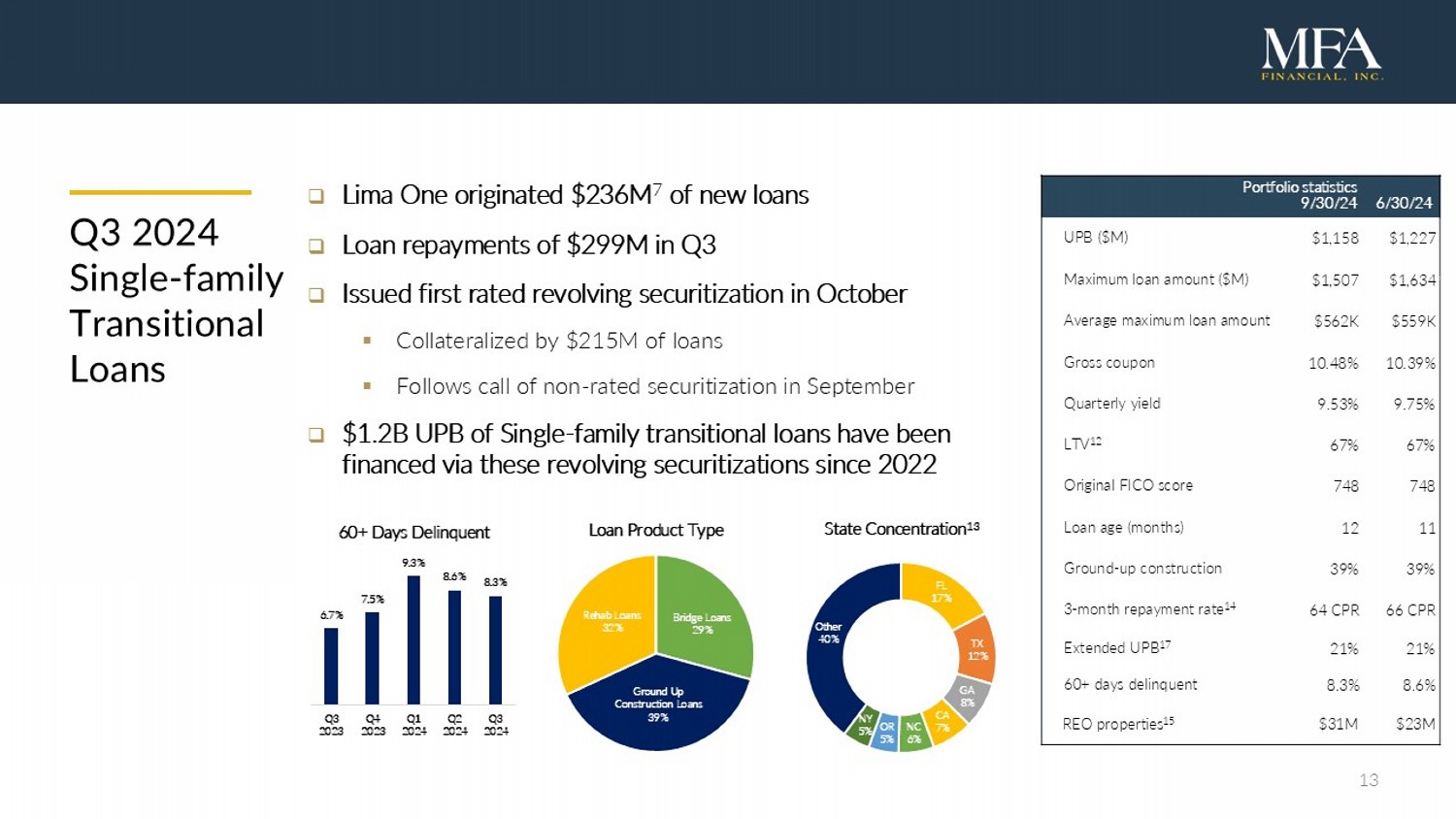

13 6/30/24 Portfolio s tatistics 9/30/24 $1,227 d $1,158 UPB ($M) $1,634 f $1,507 Maximum loan amount ($M) $559K d $562K Average maximum loan amount 10.39% d 10.48% Gross coupon 9.75% d 9.53% Quarterly yield 67% d 67% LTV 12 748 d 748 Original FICO score 11 d 12 Loan age (months) 39% d 39% Ground - up construction 66 CPR d 64 CPR 3 - month repayment rate 14 21% d 21% Extended UPB 17 8.6% d 8.3% 60+ days delinquent $23M d $31M REO properties 15 Q3 2024 Single - family Transitional Loans □ Lima One originated $236M 7 of new loans □ Loan repayments of $299M in Q3 □ Issued first rated revolving securitization in October ▪ Collateralized by $215M of loans ▪ Follows call of non - rated securitization in September □ $1.2B UPB of Single - family transitional loans have been financed via these revolving securitizations since 2022 Bridge Loans 29% Ground Up Construction Loans 39% Rehab Loans 32% Loan Product Type FL 17% TX 12% GA 8% CA 7% NC 6% OR 5% NY 5% Other 40% State Concentration 13 6.7% 7.5% 9.3% 8.6% 8.3% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 60+ Days Delinquent

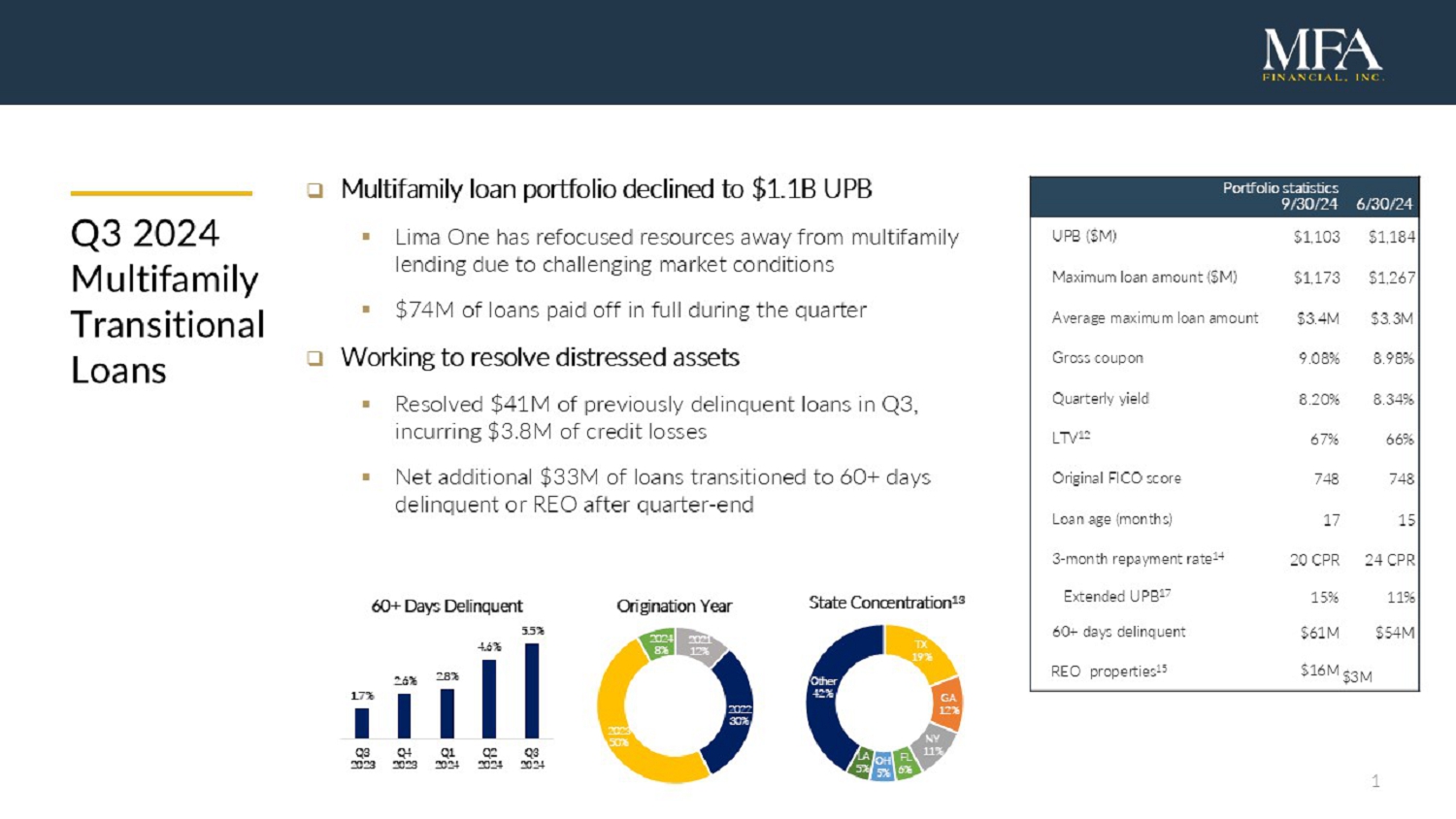

14 6/30/24 Portfolio s tatistics 9/30/24 $1,184 d $1,103 UPB ($M) $1,267 d $1,173 Maximum loan amount ($M) $3.3M d $3.4M Average maximum loan amount 8.98% d 9.08% Gross coupon 8.34% d 8.20% Quarterly yield 66% d 67% LTV 12 748 d 748 Original FICO score 15 d 17 Loan age (months) 24 CPR d 20 CPR 3 - month repayment rate 14 11% s 15% Extended UPB 17 $54M d $61M 60+ days delinquent $ 3 M $16M REO properties 15 Q3 2024 Multifamily Transitional Loans □ Multifamily loan portfolio declined to $1.1B UPB ▪ Lima One has refocused resources away from multifamily lending due to challenging market conditions ▪ $74M of loans paid off in full during the quarter □ Working to resolve distressed assets ▪ Resolved $41M of previously delinquent loans in Q3, incurring $3.8M of credit losses ▪ Additional $32M of loans transitioned to 60+ days delinquent after quarter - end TX 19% GA 12% NY 11% FL 6% OH 5% LA 5% Other 42% State Concentration 13 2021 12% 2022 30% 2023 50% 2024 8% Origination Year 1.7% 2.6% 2.8% 4.6% 5.5% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 60+ Days Delinquent

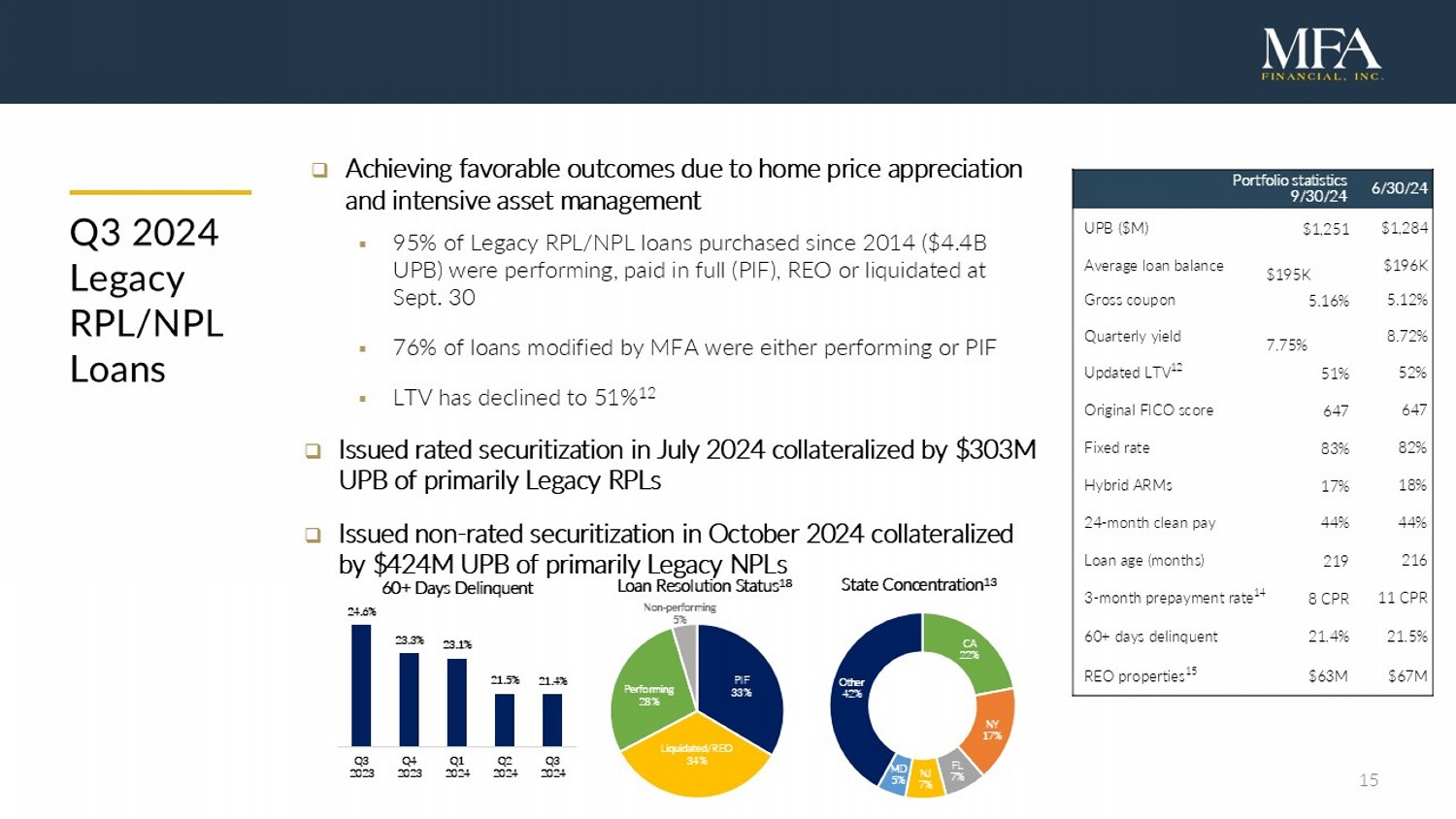

15 Q3 2024 Legacy RPL/NPL Loans □ Achieving favorable outcomes due to home price appreciation and intensive asset management ▪ 95% of Legacy RPL/NPL loans purchased since 2014 ($4.4B UPB) were performing, paid in full (PIF), REO or liquidated at Sept. 30 ▪ 76% of loans modified by MFA were either performing or PIF ▪ LTV has declined to 51% 12 □ Issued rated securitization in July 2024 collateralized by $303M UPB of primarily Legacy RPLs □ Issued non - rated securitization in October 2024 collateralized by $424M UPB of primarily Legacy NPLs 6/30/24 P ortfolio s tatistics 9/30/24 $1,284 1 $1,251 UPB ($M) $196K 1 $195K Average loan balance 5.12% 1 5.16% Gross coupon 8.72% 1 7.75% Quarterly yield 52% 1 51% Updated LTV 12 647 1 647 Original FICO score 82% 1 83% Fixed rate 18% 1 17% Hybrid ARMs 44% 1 44% 24 - month clean pay 216 1 219 Loan age (months) 11 CPR 1 8 CPR 3 - month prepayment rate 14 21.5% 1 21.4% 60+ days delinquent $67M 1 $63M REO properties 15 CA 22% NY 17% FL 7% NJ 7% MD 5% Other 42% State Concentration 13 PIF 33% Liquidated/REO 34% Performing 28% Non - performing 5% Loan Resolution Status 18 24.6% 23.3% 23.1% 21.5% 21.4% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 60+ Days Delinquent

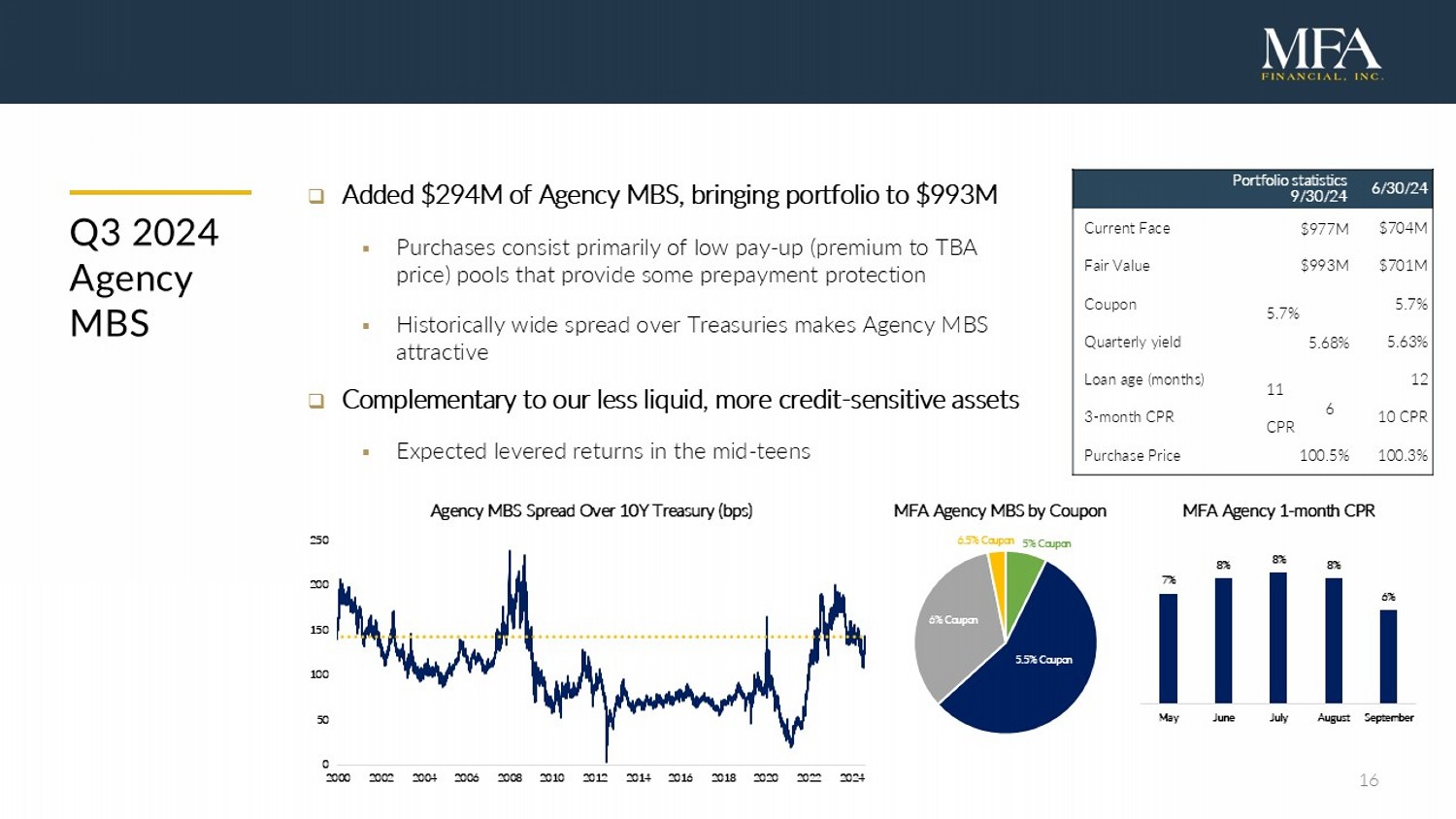

16 Q3 2024 Agency MBS □ Added $294M of Agency MBS, bringing portfolio to $993M ▪ Purchases consist primarily of low pay - up (premium to TBA price) pools that provide some prepayment protection ▪ Historically wide spread over Treasuries makes Agency MBS attractive □ Complementary to our less liquid, more credit - sensitive assets ▪ Expected levered returns in the mid - teens 5% Coupon 5.5% Coupon 6% Coupon 6.5% Coupon MFA Agency MBS by Coupon 6/30/24 P ortfolio s tatistics 9/30/24 $704M 1 $977M Current Face $701M 1 $993M Fair Value 5.7% 1 5.7% Coupon 5.63% 1 5.68% Quarterly yield 12 1 11 Loan age (months) 10 CPR 1 6 CPR 3 - month CPR 100.3% 1 100.5% Purchase Price 7% 8% 8% 8% 6% May June July August September MFA Agency 1 - month CPR 0 50 100 150 200 250 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 Agency MBS Spread Over 10Y Treasury (bps)

17 Appendix James Casebere , Landscape with Houses ( Dutchess County, NY) #2, 2010 (detail)

18 MFA Financial Overview □ MFA Financial, Inc. (NYSE: MFA) is an internally managed real estate investment trust (REIT) that invests in U.S. residential mortgage loans and mortgage - backed securities □ MFA focuses primarily on mortgage subsectors in which it tries to avoid direct competition with banks and government - sponsored enterprises □ MFA owns a diversified portfolio of business purpose loans (BPLs), non - qualified mortgage (Non - QM) loans, re - performing/non - performing loans (Legacy RPL/NPLs) and residential mortgage - backed securities □ In 2021, MFA acquired Lima One Capital, a leading nationwide BPL originator and servicer with over $10B 7 in originations since its formation in 2010 □ MFA originates BPLs directly through Lima One and acquires Non - QM loans through flow and mini - bulk arrangements with a select group of originators with which it holds strong relationships □ MFA operates a leading residential credit securitization platform with $9.8B of issuance since inception □ MFA has deep expertise in residential credit as well as a long history of investing in new asset classes when compelling opportunities arise □ Since its IPO in 1998, MFA has distributed $4.8 billion of dividends to its stockholders

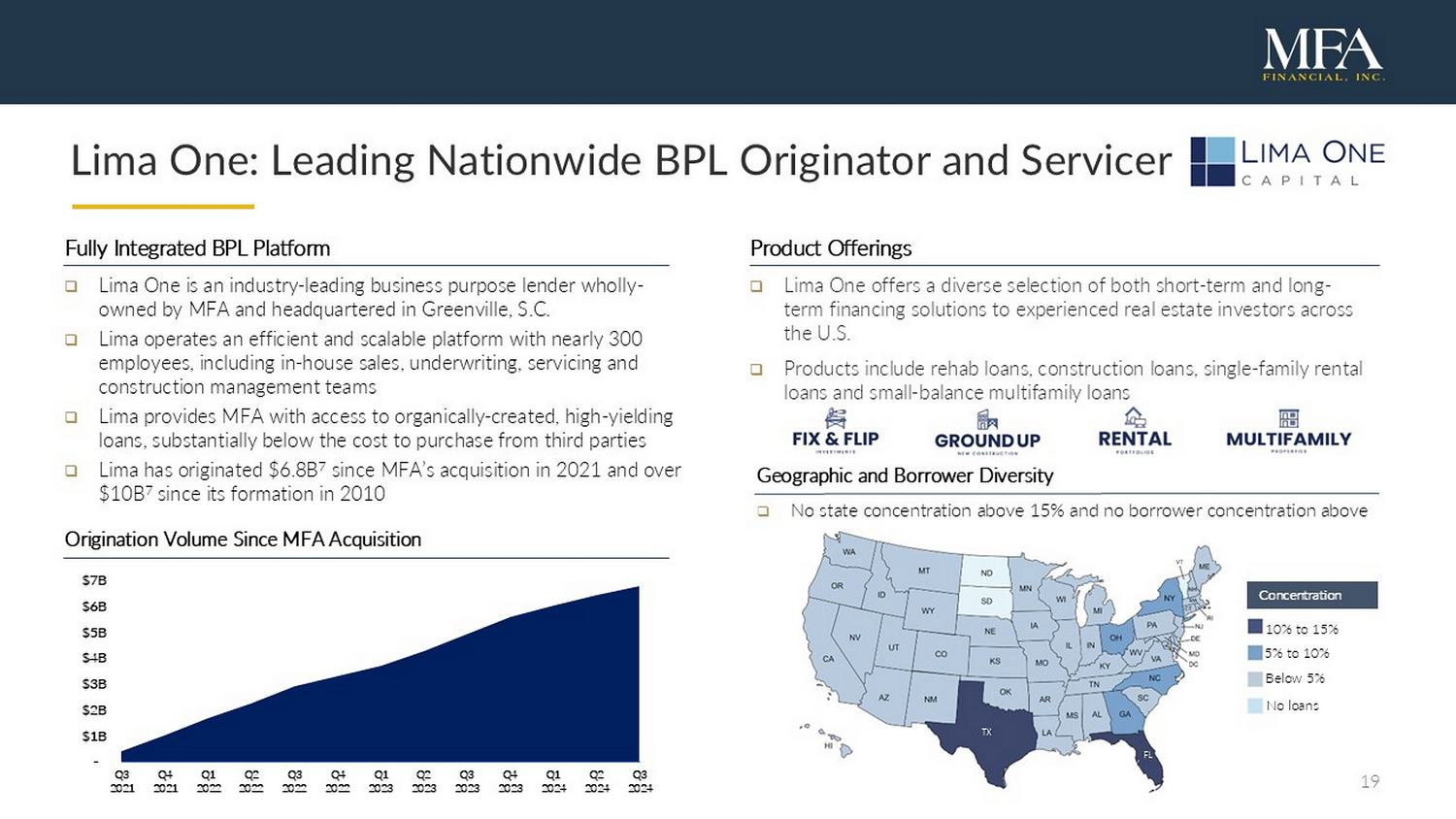

19 Lima One: Leading Nationwide BPL Originator and Servicer Product Offerings □ Lima One offers a diverse selection of both short - term and long - term financing solutions to experienced real estate investors across the U.S. □ Products include rehab loans, construction loans, single - family rental loans and small - balance multifamily loans Fully Integrated BPL Platform □ Lima One is an industry - leading business purpose lender wholly - owned by MFA and headquartered in Greenville, S.C. □ Lima operates an efficient and scalable platform with nearly 300 employees, including in - house sales, underwriting, servicing and construction management teams □ Lima provides MFA with access to organically - created, high - yielding loans, substantially below the cost to purchase from third parties □ Lima has originated $6.8 B 7 since MFA’s acquisition in 2021 and over $10B 7 since its formation in 2010 Geographic and Borrower Diversity □ No state concentration above 15% and no borrower concentration above 2% Concentration 10% to 15% 5% to 10% Below 5% No loans TX FL TX FL Origination Volume Since MFA Acquisition - $1B $2B $3B $4B $5B $6B $7B Q3 2021 Q4 2021 Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024

20 Book Value Potential Upside □ Economic book value has $1.41 per share of potential upside ▪ Many of our Non - QM and SFR loans are marked at a discount to par due to the impact of higher interest rates ▪ We recoup that discount as borrowers make scheduled principal payments and as loans pay off □ Economic book value would be $15.87 per share if those loans and their associated securitized debt were repaid at par ▪ Any realized credit losses or loan sales below par would reduce potential upside $4.84 $1.41 potential upside $14.46 EBV $4 $6 $8 $10 $12 $14 $16 $18 MFA Stock Price 9/30 EBV 9/30 Loan Portfolio Discount to Par Securitized Debt Discount to Par Potential EBV Potential Upside in Economic Book Value 19 $14.46 $12.72 $2.56 $(1.15)

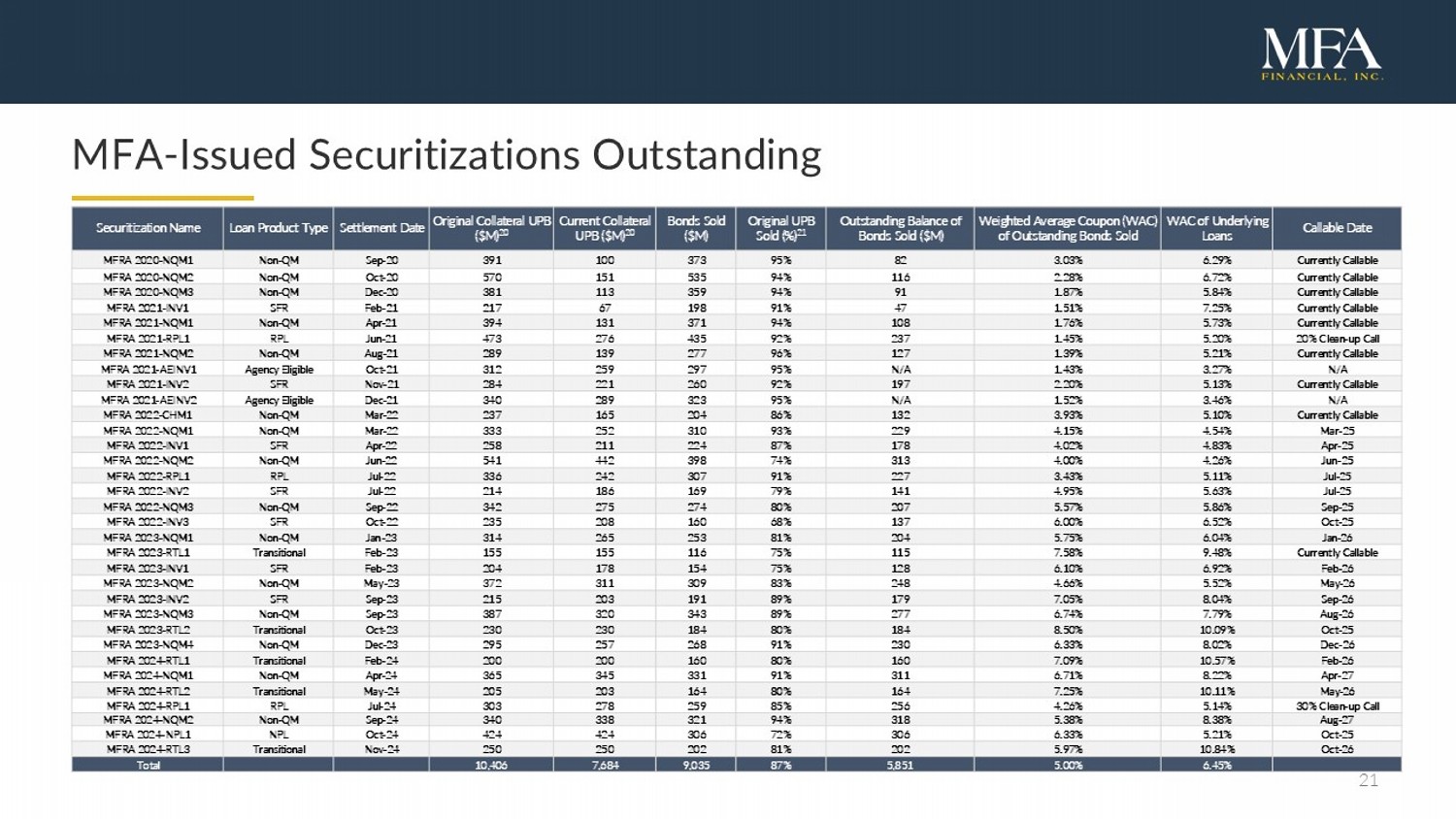

21 MFA - Issued Securitizations Outstanding Callable Date WAC of Underlying Loans Weighted Average Coupon (WAC) of Outstanding Bonds Sold Outstanding Balance of Bonds Sold ($M) Original UPB Sold (%) 21 Bonds Sold ($M) Current Collateral UPB ($M) 20 Original Collateral UPB ($M) 20 Settlement Date Loan Product Type Securitization Name Currently Callable 6.29% 3.03% 82 95% 373 100 391 Sep - 20 Non - QM MFRA 2020 - NQM1 Currently Callable 6.72% 2.28% 116 94% 535 151 570 Oct - 20 Non - QM MFRA 2020 - NQM2 Currently Callable 5.84% 1.87% 91 94% 359 113 381 Dec - 20 Non - QM MFRA 2020 - NQM3 Currently Callable 7.25% 1.51% 47 91% 198 67 217 Feb - 21 SFR MFRA 2021 - INV1 Currently Callable 5.73% 1.76% 108 94% 371 131 394 Apr - 21 Non - QM MFRA 2021 - NQM1 20% Clean - up Call 5.20% 1.45% 237 92% 435 276 473 Jun - 21 RPL MFRA 2021 - RPL1 Currently Callable 5.21% 1.39% 127 96% 277 139 289 Aug - 21 Non - QM MFRA 2021 - NQM2 N/A 3.27% 1.43% N/A 95% 297 259 312 Oct - 21 Agency Eligible MFRA 2021 - AEINV1 Currently Callable 5.13% 2.20% 197 92% 260 221 284 Nov - 21 SFR MFRA 2021 - INV2 N/A 3.46% 1.52% N/A 95% 323 289 340 Dec - 21 Agency Eligible MFRA 2021 - AEINV2 Currently Callable 5.10% 3.93% 132 86% 204 165 237 Mar - 22 Non - QM MFRA 2022 - CHM1 Mar - 25 4.54% 4.15% 229 93% 310 252 333 Mar - 22 Non - QM MFRA 2022 - NQM1 Apr - 25 4.83% 4.02% 178 87% 224 211 258 Apr - 22 SFR MFRA 2022 - INV1 Jun - 25 4.26% 4.00% 313 74% 398 442 541 Jun - 22 Non - QM MFRA 2022 - NQM2 Jul - 25 5.11% 3.43% 227 91% 307 242 336 Jul - 22 RPL MFRA 2022 - RPL1 Jul - 25 5.63% 4.95% 141 79% 169 186 214 Jul - 22 SFR MFRA 2022 - INV2 Sep - 25 5.86% 5.57% 207 80% 274 275 342 Sep - 22 Non - QM MFRA 2022 - NQM3 Oct - 25 6.52% 6.00% 137 68% 160 208 235 Oct - 22 SFR MFRA 2022 - INV3 Jan - 26 6.04% 5.75% 204 81% 253 265 314 Jan - 23 Non - QM MFRA 2023 - NQM1 Currently Callable 9.48% 7.58% 115 75% 116 155 155 Feb - 23 Transitional MFRA 2023 - RTL1 Feb - 26 6.92% 6.10% 128 75% 154 178 204 Feb - 23 SFR MFRA 2023 - INV1 May - 26 5.52% 4.66% 248 83% 309 311 372 May - 23 Non - QM MFRA 2023 - NQM2 Sep - 26 8.04% 7.05% 179 89% 191 203 215 Sep - 23 SFR MFRA 2023 - INV2 Aug - 26 7.79% 6.74% 277 89% 343 320 387 Sep - 23 Non - QM MFRA 2023 - NQM3 Oct - 25 10.09% 8.50% 184 80% 184 230 230 Oct - 23 Transitional MFRA 2023 - RTL2 Dec - 26 8.02% 6.33% 230 91% 268 257 295 Dec - 23 Non - QM MFRA 2023 - NQM4 Feb - 26 10.57% 7.09% 160 80% 160 200 200 Feb - 24 Transitional MFRA 2024 - RTL1 Apr - 27 8.22% 6.71% 311 91% 331 345 365 Apr - 24 Non - QM MFRA 2024 - NQM1 May - 26 10.11% 7.25% 164 80% 164 203 205 May - 24 Transitional MFRA 2024 - RTL2 30% Clean - up Call 5.14% 4.26% 256 85% 259 278 303 Jul - 24 RPL MFRA 2024 - RPL1 Aug - 27 8.38% 5.38% 318 94% 321 338 340 Sep - 24 Non - QM MFRA 2024 - NQM2 Oct - 25 5.21% 6.33% 306 72% 306 424 424 Oct - 24 NPL MFRA 2024 - NPL1 Oct - 26 10.84% 5.97% 202 81% 202 250 250 Nov - 24 Transitional MFRA 2024 - RTL3 6.45% 5.00% 5,851 87% 9,035 7,684 10,406 Total

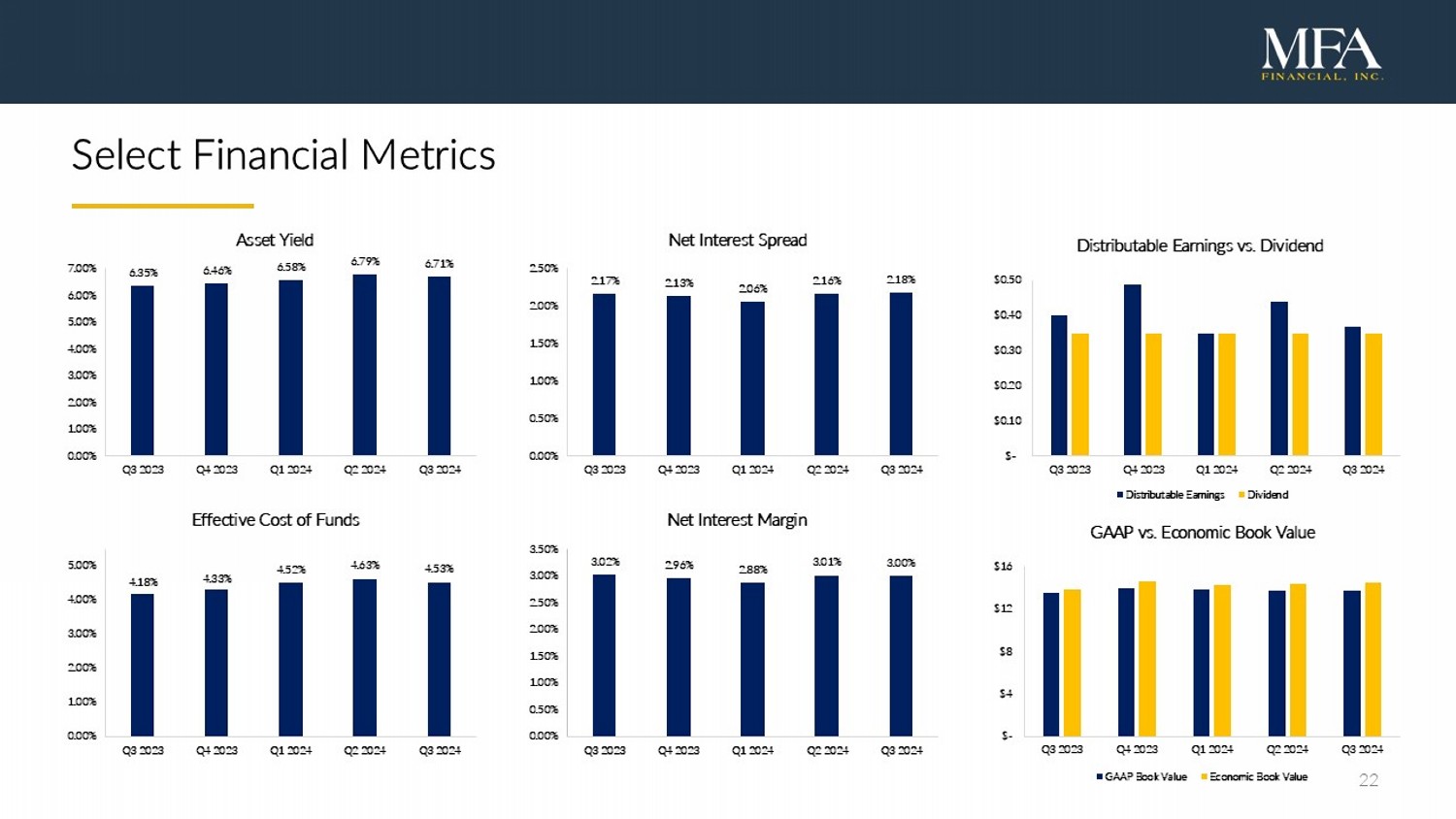

22 Select Financial Metrics 6.35% 6.46% 6.58% 6.79% 6.71% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Asset Yield 2.17% 2.13% 2.06% 2.16% 2.18% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Net Interest Spread 3.02% 2.96% 2.88% 3.01% 3.00% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Net Interest Margin 4.18% 4.33% 4.52% 4.63% 4.53% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Effective Cost of Funds $- $0.10 $0.20 $0.30 $0.40 $0.50 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 Distributable Earnings vs. Dividend Distributable Earnings Dividend $- $4 $8 $12 $16 Q3 2023 Q4 2023 Q1 2024 Q2 2024 Q3 2024 GAAP vs. Economic Book Value GAAP Book Value Economic Book Value

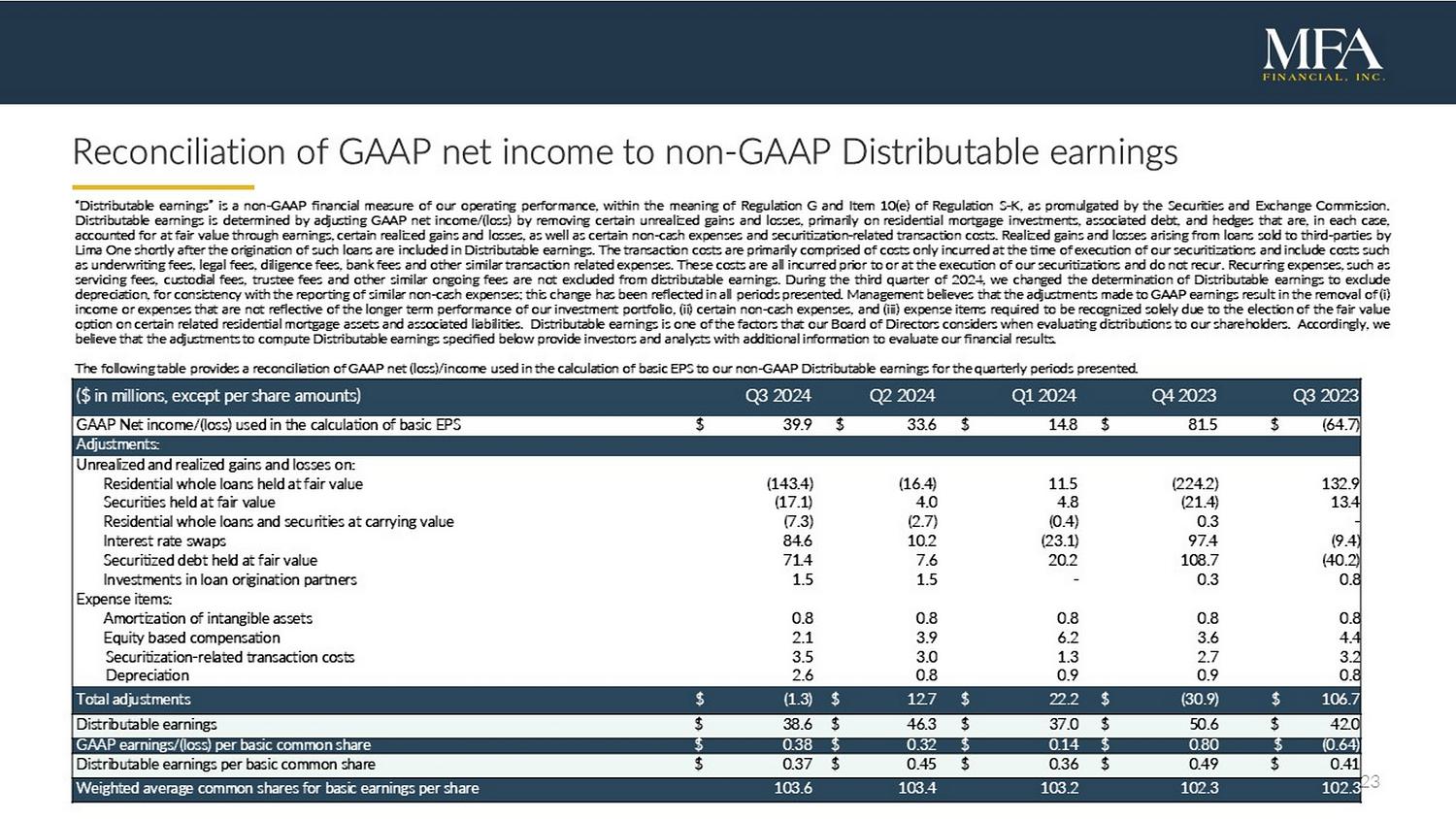

23 Reconciliation of GAAP net income to non - GAAP Distributable earnings “Distributable earnings” is a non - GAAP financial measure of our operating performance, within the meaning of Regulation G and Item 10 (e) of Regulation S - K, as promulgated by the Securities and Exchange Commission . Distributable earnings is determined by adjusting GAAP net income/(loss) by removing certain unrealized gains and losses, primarily on residential mortgage investments, associated debt, and hedges that are, in each case, accounted for at fair value through earnings, certain realized gains and losses, as well as certain non - cash expenses and securitization - related transaction costs . Realized gains and losses arising from loans sold to third - parties by Lima One shortly after the origination of such loans are included in Distributable earnings . The transaction costs are primarily comprised of costs only incurred at the time of execution of our securitizations and include costs such as underwriting fees, legal fees, diligence fees, bank fees and other similar transaction related expenses . These costs are all incurred prior to or at the execution of our securitizations and do not recur . Recurring expenses, such as servicing fees, custodial fees, trustee fees and other similar ongoing fees are not excluded from distributable earnings . During the third quarter of 2024 , we changed the determination of Distributable earnings to exclude depreciation, for consistency with the reporting of similar non - cash expenses ; this change has been reflected in all periods presented . Management believes that the adjustments made to GAAP earnings result in the removal of ( i ) income or expenses that are not reflective of the longer term performance of our investment portfolio, (ii) certain non - cash expenses, and (iii) expense items required to be recognized solely due to the election of the fair value option on certain related residential mortgage assets and associated liabilities . Distributable earnings is one of the factors that our Board of Directors considers when evaluating distributions to our shareholders . Accordingly, we believe that the adjustments to compute Distributable earnings specified below provide investors and analysts with additional information to evaluate our financial results . The following table provides a reconciliation of GAAP net (loss)/income used in the calculation of basic EPS to our non - GAAP Distributable earnings for the quarterly periods presented . Q3 202 3 Q4 202 3 Q1 202 4 Q2 202 4 Q3 202 4 ( $ i n m illions, e xcept p er s hare a mounts) $ (64.7) $ 81.5 $ 14.8 $ 33.6 $ 39.9 GAAP Net income/(loss) used in the calculation of basic EPS Adjustments: Unrealized and realized gains and losses on: 132.9 (224.2) 11.5 (16.4) (143.4) Residential whole loans held at fair value 13.4 (21.4) 4.8 4.0 (17.1) Securities held at fair value - 0.3 (0.4) (2.7) (7.3) Residential whole loans and securities at carrying value (9.4) 97.4 (23.1) 10.2 84.6 Interest rate swaps (40.2) 108.7 20.2 7.6 71.4 Securitized debt held at fair value 0.8 0.3 - 1.5 1.5 Investments in loan origination partners Expense items: 0.8 0.8 0.8 0.8 0.8 Amortization of intangible assets 4.4 3.6 6.2 3.9 2.1 Equity based compensation 3.2 2.7 1.3 3.0 3.5 Securitization - related transaction costs 0.8 0.9 0.9 0.8 2.6 Depreciation $ 106.7 $ (30.9) $ 22.2 $ 12.7 $ (1.3) Total adjustments $ 42.0 $ 50.6 $ 37.0 $ 46.3 $ 38.6 Distributable earnings $ (0.64) $ 0.80 $ 0.14 $ 0.32 $ 0.38 GAAP earnings/(loss) per basic common share $ 0.41 $ 0.49 $ 0.36 $ 0.45 $ 0.37 Distributable earnings per basic common share 10 2.3 102.3 103.2 103.4 103.6 Weighted average common shares for basic earnings per share

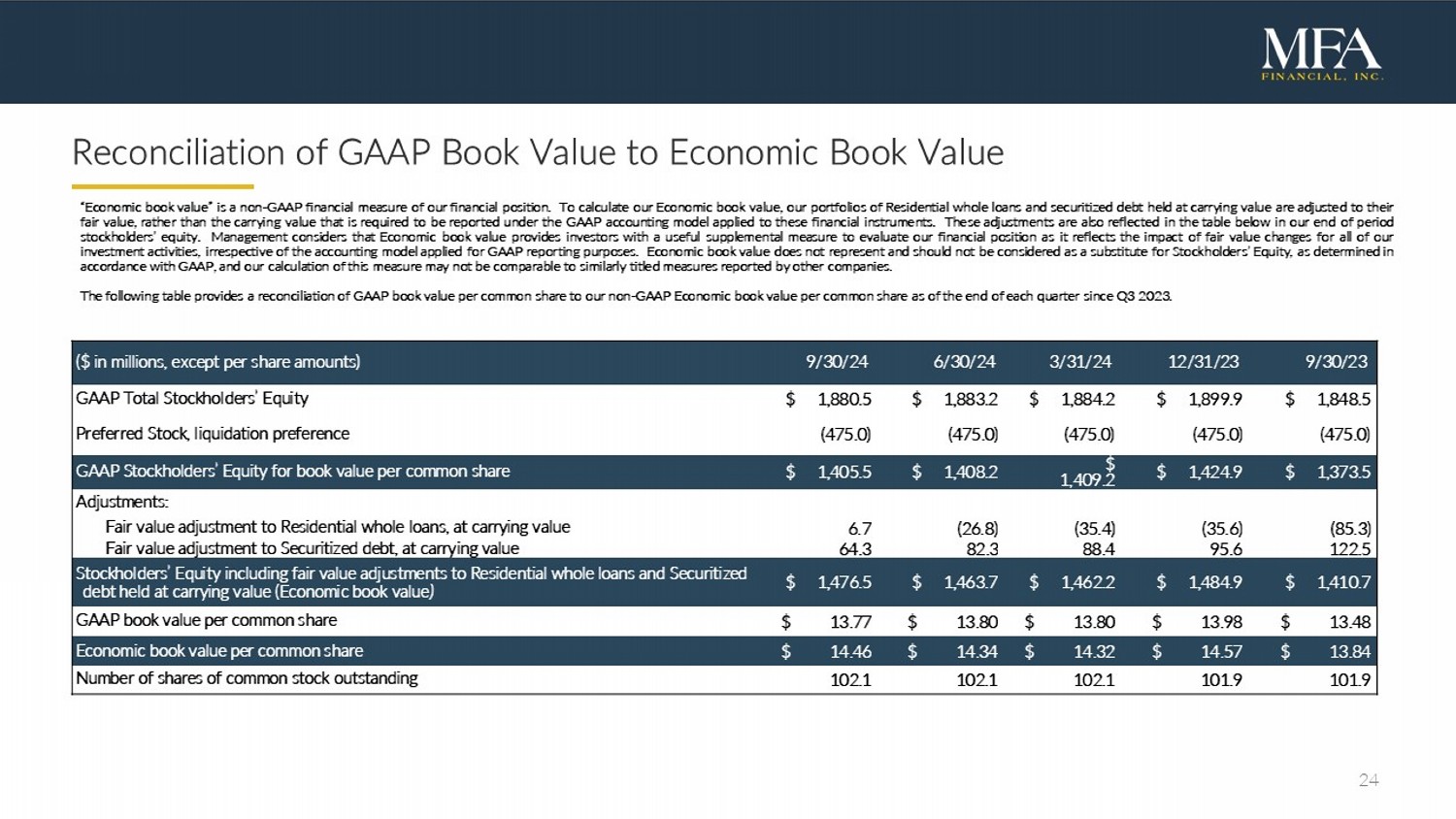

24 Reconciliation of GAAP Book Value to Economic Book Value “Economic book value” is a non - GAAP financial measure of our financial position . To calculate our Economic book value, our portfolios of Residential whole loans and securitized debt held at carrying value are adjusted to their fair value, rather than the carrying value that is required to be reported under the GAAP accounting model applied to these financial instruments . These adjustments are also reflected in the table below in our end of period stockholders’ equity . Management considers that Economic book value provides investors with a useful supplemental measure to evaluate our financial position as it reflects the impact of fair value changes for all of our investment activities, irrespective of the accounting model applied for GAAP reporting purposes . Economic book value does not represent and should not be considered as a substitute for Stockholders’ Equity, as determined in accordance with GAAP, and our calculation of this measure may not be comparable to similarly titled measures reported by other companies . The following table provides a reconciliation of GAAP book value per common share to our non - GAAP Economic book value per common share as of the end of each quarter since Q 3 2023 . 9/30 /2 3 12/31 /2 3 3/31/24 6/30/24 9/30/24 ($ i n millions, except per share amounts) $ 1,848.5 $ 1,899.9 $ 1,884.2 $ 1,883.2 $ 1,880.5 GAAP Total Stockholders’ Equity (475.0) (475.0) (475.0) (475.0) (475.0) Preferred Stock, liquidation preference $ 1,373.5 $ 1,424.9 $ 1,409.2 $ 1,408.2 $ 1,405.5 GAAP Stockholders’ Equity for book value per common share Adjustments: (85.3) (35.6) (35.4) (26.8) 6.7 Fair value adjustment to Residential whole loans, at carrying value 122.5 95.6 88.4 82.3 64.3 Fair value adjustment to Securitized debt, at carrying value $ 1,410.7 $ 1,484.9 $ 1,462.2 $ 1,463.7 $ 1,476.5 Stockholders’ Equity including fair value adjustments to Residential whole loans and Securitized debt held at carrying value (Economic book value ) $ 13.48 $ 13.98 $ 13.80 $ 13.80 $ 13.77 GAAP book value per common share $ 13.84 $ 14.57 $ 14.32 $ 14.34 $ 14.46 Economic book value per common share 101.9 101.9 102.1 102.1 102.1 Number of shares of common stock outstanding

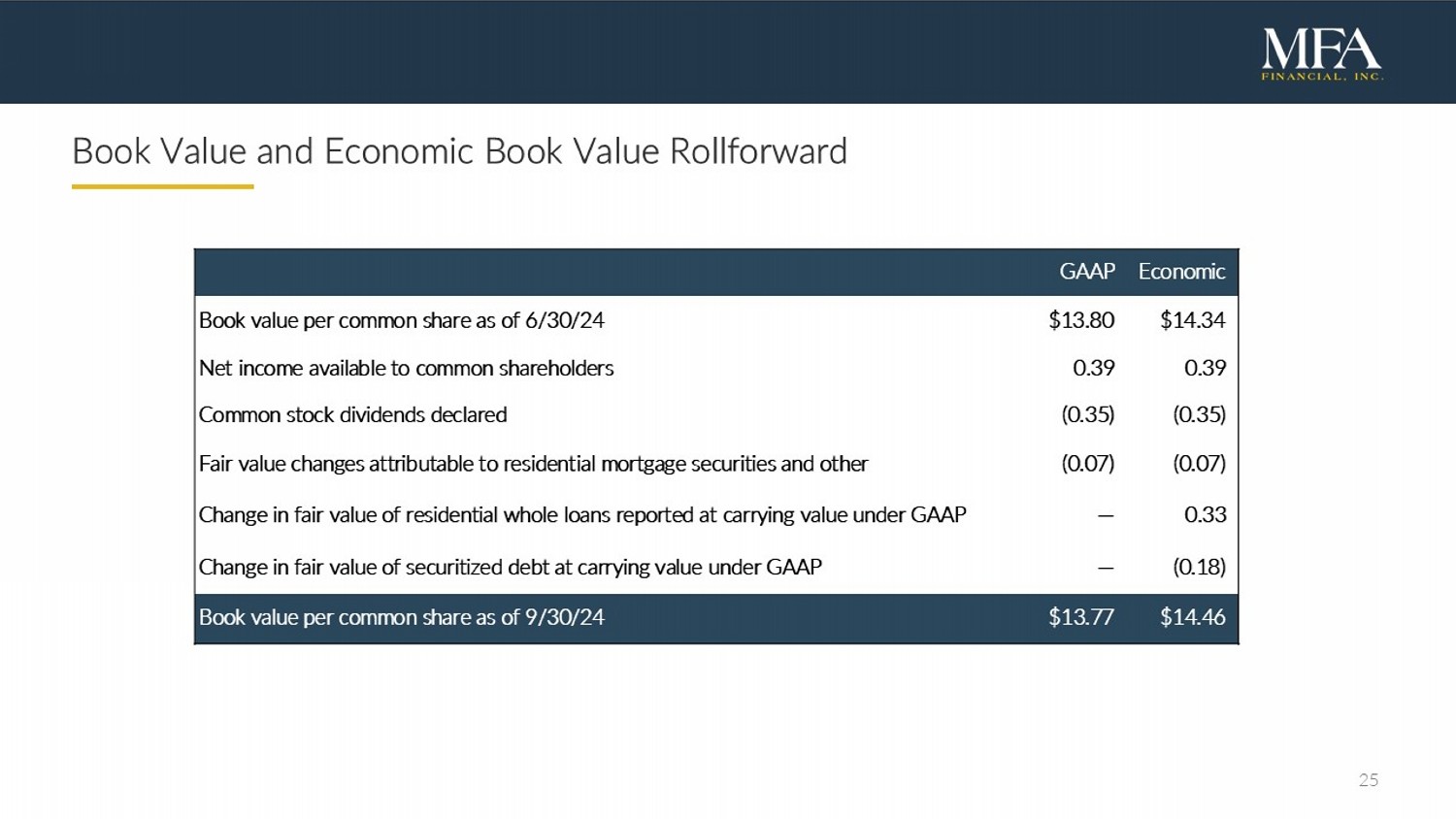

25 Book Value and Economic Book Value Rollforward Economic GAAP $14.34 $13.80 Book value per common share as of 6/30/24 0.39 0.39 Net income available to common shareholders (0. 35 ) (0. 35 ) Common stock dividends declared (0.07) (0.07) Fair value changes attributable to residential mortgage securities and other 0.33 — Change in fair value of residential whole loans reported at carrying value under GAAP (0.18) — Change in fair value of securitized debt at carrying value under GAAP $ 14.46 $ 13.77 Book value per common share as of 9/30/24

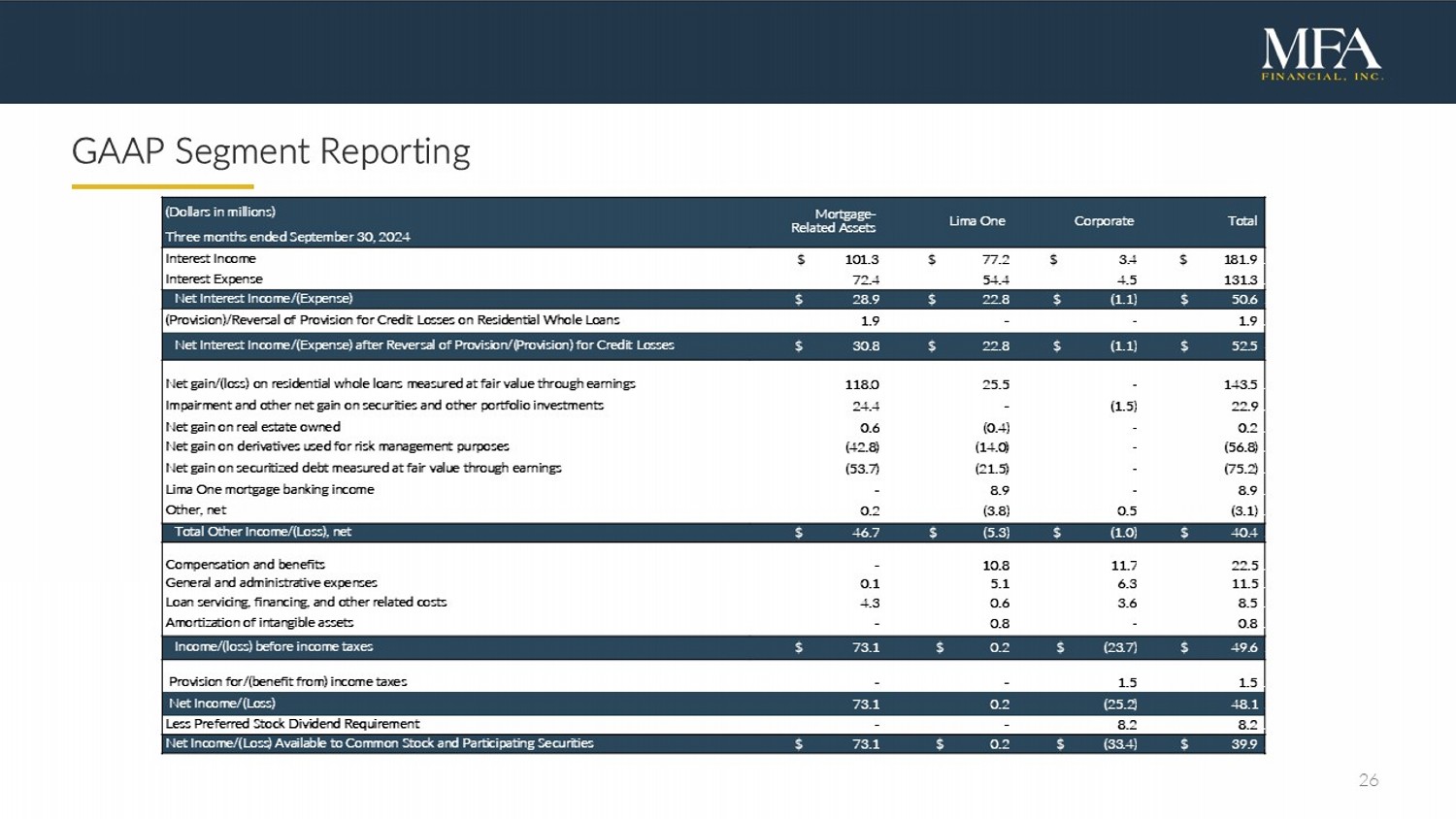

26 GAAP Segment Reporting Total d Corporate Lima One Mortgage - Related Assets (Dollars in m illions) Three months ended September 30, 2024 $ 181.9 1 $ 3.4 $ 77.2 $ 101.3 Interest Income 131.3 1 4.5 54.4 72.4 Interest Expense $ 50.6 1 $ (1.1) $ 22.8 $ 28.9 Net Interest Income /(Expense) 1.9 1 - - 1.9 (Provision)/Reversal of Provision for Credit Losses on Residential Whole Loans $ 52.5 4 $ (1.1) $ 22.8 $ 30.8 Net Interest Income /(Expense) after Reversal of Provision/( Provision ) for Credit Losses 143.5 1 - 25.5 118.0 Net gain/(loss) on residential whole loans measured at fair value through earnings 22.9 1 (1.5) - 24.4 Impairment and other net gain on securities and other portfolio investments 0.2 1 - (0.4) 0.6 Net gain on real estate owned (56.8) 1 - (14.0) (42.8) Net gain on derivatives used for risk management purposes (75.2) 1 - (21.5) (53.7) Net gain on securitized debt measured at fair value through earnings 8.9 1 - 8.9 - Lima One mortgage banking income (3.1) 1 0.5 (3.8) 0.2 Other, net $ 40.4 1 $ (1.0) $ (5.3) $ 46.7 Total Other Income/(Loss) , net 22.5 1 11.7 10.8 - Compensation and benefits 11.5 1 6.3 5.1 0.1 General and administrative expenses 8.5 1 3.6 0.6 4.3 Loan servicing, financing, and other related costs 0.8 1 - 0.8 - Amortization of intangible assets $ 49.6 1 $ (23.7) $ 0.2 $ 73.1 Income/(loss) before income taxes 1.5 1 1.5 - - Provision for/(benefit from) income taxes 48.1 1 (25.2) 0.2 73.1 Net Income/(Loss) 8.2 1 8.2 - - Less Preferred Stock Dividend Requirement $ 39.9 1 $ (33.4) $ 0.2 $ 73.1 Net Income/( Loss ) Available to Common Stock and Participating Securities

27 Endnotes 1) Purchased value of all residential whole loans acquired by MFA since 2014. 2) Economic book value is a non - GAAP financial measure. Refer to slide 24 for further information regarding the calculation of thi s measure and a reconciliation to GAAP book value. 3) GAAP net income presented per basic common share. 4) Distributable earnings is a non - GAAP financial measure. Refer to slide 23 for further information regarding the calculation of this measure and a reconciliation to GAAP net income. Distributable earnings presented per basic common share. 5) Recourse leverage is the ratio of MFA’s financing liabilities (excluding non - recourse debt) to net equity. Including Securitize d Debt, MFA’s overall leverage ratio at September 30, 2024 was 4.8x. 6) Total economic return is calculated as the quarterly change in Economic Book Value (EBV) plus common dividends declared durin g t he quarter divided by EBV at the start of the quarter. 7) Origination amount is based on the maximum loan amount, which includes amounts initially funded plus any committed but undraw n a mounts. 8) Includes $196M of funded originations during Q3 plus $133M of draws funded during Q3 on previously originated Transitional lo ans . 9) Amounts presented reflect the aggregation of fair value and carrying value amounts as presented in MFA’s consolidated balance sh eet at September 30, 2024. 10) Non - MTM refers to financing arrangements not subject to margin calls based on changes in the fair value of the financed resident ial whole loans. Such agreements may experience changes in advance rates or collateral eligibility as a result of factors such as changes in the delinquency statu s o f the financed residential whole loans. 11) Swap variable receive rate is the Secured Overnight Financing Rate (SOFR). 12) LTV reflects principal amortization and estimated home price appreciation (or depreciation) since acquisition. Zillow Home V alu e Index (ZHVI) is utilized to estimate updated LTVs for Non - QM, SFR and Legacy RPL/NPL assets. For Transitional loans, LTV reflects either the current UPB divided by the most recen t as - is property valuation available or the maximum UPB divided by the most recent after repaired value (ARV) available. 13) State concentration measured by loan balance. All states in “Other” category have concentrations below 5%. 14) CPR includes all principal repayments. 15) Balance sheet carrying value of REO properties at September 30, 2024. 16) Weighted average debt service coverage ratio (DSCR) at time of origination. 17) Percentage of loan portfolio extended beyond original maturity date as of September 30, 2024. 18) Represents status at September 30, 2024 of all Legacy RPL/NPL loans ever acquired. Non - performing status includes all active lo ans greater than 60 days delinquent. Liquidated/REO status includes both sold and active REO properties as well as short payoff liquidations and loans sold to thi rd - parties. 19) Transitional loans are excluded from the calculation of potential upside in Economic book value. 20) Collateral UPB includes cash for Transitional loan securitizations. 21) Bonds sold relative to certificates issued.